All Financial Horse does in his free time during the week is read financial news. With this new initiative, hopefully some good can come out of it. During the week, I post articles that I enjoyed on the Facebook group (do join if you want a sneak peak), and every Sunday I will collate the links for readers. I also take the opportunity to address queries from readers, or share any thoughts that I have for the week. If you enjoy this post, do share your thoughts in the comments below!

Weekly Thoughts from Financial Horse

Angry Email from Autowealth

This week’s highlight features an angry email from Autowealth. Apparently the Excel spreadsheet sent to me by StashAway in a previous post contained certain inaccuracies in their fee computation (thanks a lot StashAway).

Anyway, Autowealth reached out to me to point out the inaccuracy, and I have extracted their explanation below (with their consent, of course) for the benefit of readers. As always, I will leave my thoughts below.

To protect against myself from further angry emails, please do note the full disclaimer below:

Important:

The statements herein do not purport to be an accurate, comprehensive or exhaustive description of AutoWealth, StashAway or Smartly. They may contain technical, typographical, or photographic errors. Financial Horse does not warrant or make any representations concerning the accuracy, likely results, or reliability of the use of the materials below. If you are in any doubt as to the action you should take, you should consult your stock broker, solicitor, accountant or other professional adviser immediately.

Email from AutoWealth:

Inaccuracies on fee computations

In contrast with other robo-advisors which collect their fees at the end of each month, AutoWealth collects our fees at the end of each quarter. This is explicitly mentioned in our FAQ “How are AutoWealth’s fees and charges collected?” (https://www.autowealth.sg/faq.php)…

Despite an identical 6% projected returns, the relatively front-loaded fees meant that clients who invest with the other robo-advisors have less investment capital remaining at the end of each month to generate investment returns. Please jump to the Fee Comparison Conclusion to see the material difference in end results.

A more mainstream, data-backed comparison

StashAway provided the fee computations based on an assumption of S$2,000 monthly regular investment plan…

Based on Singapore Department of Statistics data sourced from the Ministry of Manpower, the median wage was S$4,232 incl employer CPF in 2017. Excluding employer and employee CPF, the median cash wage was S$2,894 in 2017. Therefore, an average investor who sets aside 20%~35% of his cash wage for investment is typically capable of investing about S$550~S$1,000 per month. For the fee comparison to make sense to most investors, we adopted a S$550~S$1,000 monthly regular investment plan assumption.

Fee comparison conclusion

As shown in the spreadsheet provided, clients who invest with AutoWealth achieves the highest portfolio value at the end of 30 years. This is 0.6%~1.6% higher than clients who invest with the other robo-advisors and 31.8%~32.0% higher than clients who invest through mutual funds (aka unit trusts).

Financial Horse thoughts: I’m not sure about you guys, but I’m quite sick of writing about Robos. To me the position is very clear, if you know nothing about investing and are thinking about investing in unit trusts or insurance linked products, robos are a very good alternative (of which StashAway has the best risk adjusted returns when backtested). If you are a DIY investing nut (like me), go the DIY route, you will learn far more and enjoy greater satisfaction that way.

Anyway back to the email, if you use the revised table and assumptions from Autowealth, you will end up with S$3,000 more after 30 years, which out of a S$920,000 portfolio is about 0.3%. Assumptions used are 6% returns, S$3,000 initial investment, and S$550 monthly contributions. I have attached the modified excel from Autowealth, together with the original from StashAway, for readers to independently verify (presented on an “as is” basis, please do note the disclaimer above).

However, I found it interesting that the only point AutoWealth responded to me in detail on was the Fees, when personally I felt that the difference in fees between the robos are not large. AutoWealth charges a flat 0.5% + S$18 platform fee a year, StashAway does a tiered structure as per below:

| Thresholds | Annual fee |

|

0 |

0.80% |

| 25,000 | 0.700% |

| 50,000 | 0.600% |

| 100,000 | 0.500% |

| 250,000 | 0.400% |

| 500,000 | 0.300% |

| 1,000,000 | 0.200% |

I have never advocated for picking between products based purely on fees, because things like asset allocation are equally, if not more important. When you look at the backtested returns for Autowealth vs StashAway, the stark difference points to a deeper difference in their asset allocation strategy, and I felt this was the key point to be addressed.

FAANG

In other news, a reader reached out to me to ask for my opinion on the FAANG stocks, which I felt was a very interesting question.

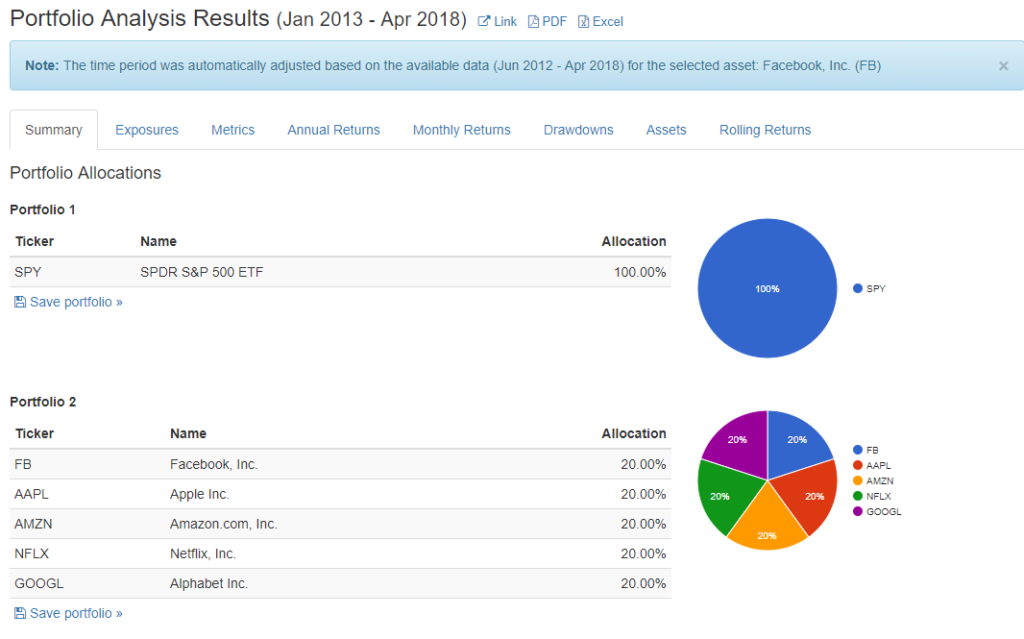

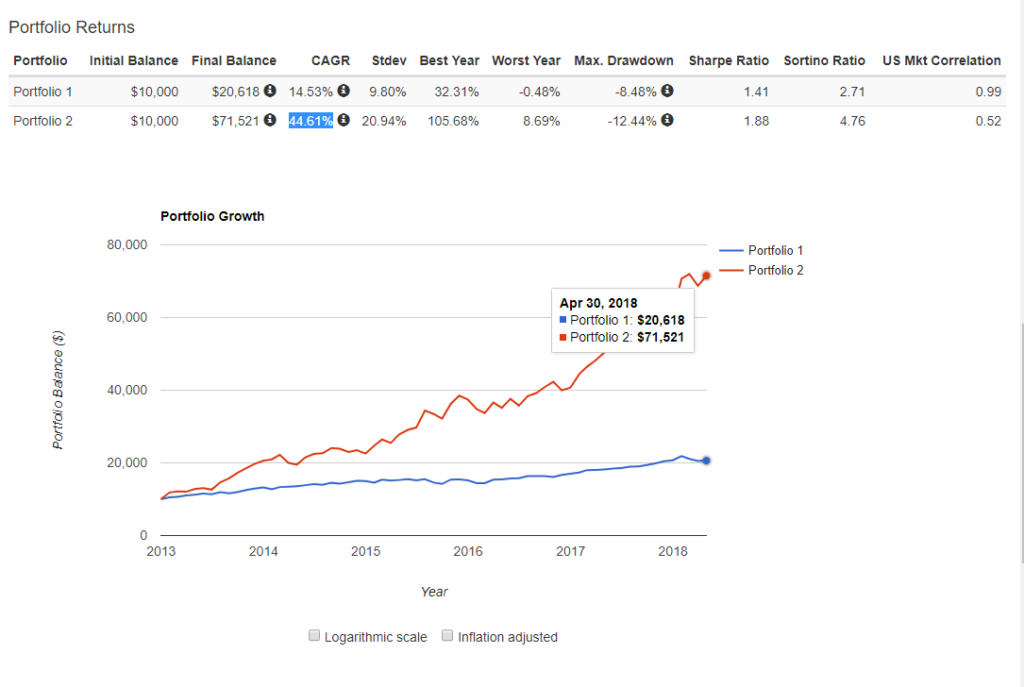

To recap, the FAANG is shortform for Facebook, Apple, Amazon, Netflix and Google (now Alphabet), which is a group of 5 tech stocks that has had mindblowing performance over the past 5 years. To illustrate, I charted the returns of a FAANG investment (even split, annual rebalancing) against the S&P500, and you can take a look at the results below (link here).

The returns for the FAANG portfolio was a truly out of this world 44.61% CAGR, while the S&P500 returned a “paltry” 14.53% CAGR. Over the past 5 years, its gotten to the point where most hedge funds are being forced to incorporate the FAANG stocks into their portfolio, for fear of underperforming.

The returns for the FAANG portfolio was a truly out of this world 44.61% CAGR, while the S&P500 returned a “paltry” 14.53% CAGR. Over the past 5 years, its gotten to the point where most hedge funds are being forced to incorporate the FAANG stocks into their portfolio, for fear of underperforming.

Personally I do not own any of the FAANG stocks directly. These days I own them indirectly via the NASDAQ (QQQ) and S&P500 (SPY) ETFs that I hold.

A lot of people would argue that given the astounding run-up that these tech stocks have had, they have a long way to fall in any recession. My response would be that true, but so has almost every stock out there. It’s very easy to single out the FAANG stocks or tech stocks given their outperformance since the GFC, and all the media attention over the catchy acronym. However, a lot of the price performance has come through genuine earnings growth. These are some of the most competitive companies in the world who are behemoths in their respective industry, controlling market share, revenue, and the top talent in their field.

My advice for the FAANG stocks, and for stocks generally, is to always decide whether you want to own a share of the company at the prevailing valuation. Forget about the FAANG status for a moment, and look purely at the business model and fundamentals of the company. Facebook is trading at 30.61 times TTM P/E, has an EV/EBITDA of 19.41, and a forward P/E of 20.23 and a PEG ratio of 0.92 (using Yahoo Finance numbers). It has been consistently growing its earnings and Monthly Average Users (MAU) every single month since its IPO. It has a huge privacy fallout from Cambridge Analytica, that may eventually manifest itself in more stringent regulations that affect its bottom line. It has a founder, Mark Zuckerberg, who seems to have greater ambitions beyond his company. It has rivals in the form of Snapchat and LinkedIn, and god knows what other startup some kid is cooking up in his garage in Silicon Valley. On this basis, are you comfortable owning this company, and participating in its growth story for the next 5 or 10 years, or even beyond?

Everybody will reach a different conclusion on the above, and no one can make the decision for you. If you are a technical trader, the identity of the company doesn’t even matter to you, you will trade based purely off signals identified by your trading model. But for investors, it is vital to evaluate each company on its own merits, and to decide whether the company is a suitable investment.

These days I no longer make specific investments in the US market unless I have a very strong conviction in any stock. At the moment, I am not particularly enamoured by any of the FAANG stocks, am I am comfortable participating in their growth through the ETFs that I hold.

Top Weekly Links

http://www.fourpillarfreedom.com/10-charts-10-insights/

(Four Pillar Freedom)

Everyone will have their own takeaways from this article, but for me, it was this:

“5. Early on in your financial journey, most of your net worth growth will come from savings. As time goes on, more and more of that growth will come from investment returns.”

You really have to see the chart to understand how powerful this is. When you are young, saving is all that matters. But as you get older, your investment returns will exceed your total savings by many multitudes. Saving and investing are powerful skills that go hand in hand.

https://www.bloomberg.com/graphics/2018-payment-systems-china-usa/

(Bloomberg)

Well researched Bloomberg article on the power of payment apps. This really illustrates why everyone from DBS to grab to fave is trying to get into this space.

Controlling payment ensures that consumers trust your network with their money. If you then start paying interest on money stored with you, you become a very attractive alternative to traditional savings accounts. You now have access to a consumer’s credit history, and from there, loans and mortgages are a logical extension. Because everything is automated from the ground up, overhead is far lower than in a traditional bank.

Currently the only way to own a slice of this pie is through Alibaba and Tencent, both of which have other core businesses.

https://www.edgeprop.sg/property-news/what-do-these-profit-making-properties-have-common

(Edgeprop)

I don’t agree 100% with this article, but I found it an interesting read nonetheless. The 5 traits pointed out: 1) longer holding period, 2) freehold tenure, 3) older properties, 4) larger area size and 5) central location seem like a no brainer that every property investor will know, but as always, the devil is in the details.

Knowing when to buy/sell, which property to pick, and how to fund the purchase are key questions that always play out better in your head than in the real world.

https://www.themacrotourist.com/posts/2018/05/23/secular/

(Macro Tourist)

Quite enjoyed this contrarian take on the bond market. While I am a bond bear myself, I do acknowledge that bonds are looking quite oversold at this point, so we may be in for a rally in bond prices in the short term.

https://www.whitecoatinvestor.com/avoid-extreme-portfolios/

(Whitecoat Investor)

It’s written for the US context (and for doctors!), but the lessons are universal.

Really illustrates the importance of having a balanced portfolio, and the importance of exposure to risk assets (tempered with diversification) when you are young.

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Insightful posts. Thanks Financial Horse.

Hi CJ How, welcome to Financial Horse, and I am glad you find this to be helpful!

Thanks for the policy update mrchow I suggest Chinese farmers are the least abused and generates the least carbon in a fully functioning society and no excise carbon crap

Its always a pleasure to come and read your thoughts on robos, for some reason I missed this one when it came out.

I hope that you continue writing on this topic every now and then.

Regards,

Keir

Smartly Founder