In last week’s article, I shared that (1) I disliked the MCT-MNACT merger, and (2) I would consider adding at $1.8 to $1.9.

By Tuesday this week, MCT had fallen to an intraday low of $1.81.

A lot of you reached out to ask if I am buying Mapletree Commercial Trust at this price.

I’ve had some time to dig deeper into MNACT’s portfolio this week. And the more I look, the more concerned I get.

So to update my views:

I now really, really dislike this merger.

I have revised my personal fair value for MCT down to $1.74 – $1.79.

Let me share why.

BTW – if you haven’t read last week’s article please do. I’m going to skip all the basics and go straight into the juicy stuff.

3 Big Problems with the Mapletree Commercial Trust Merger

There’s basically 3 big problems:

- MNACT’s portfolio is… not good?

- Valuations

- Macro Headwinds

1. Mapletree North Asia Commercial Trust (MNACT) Portfolio is… not good?

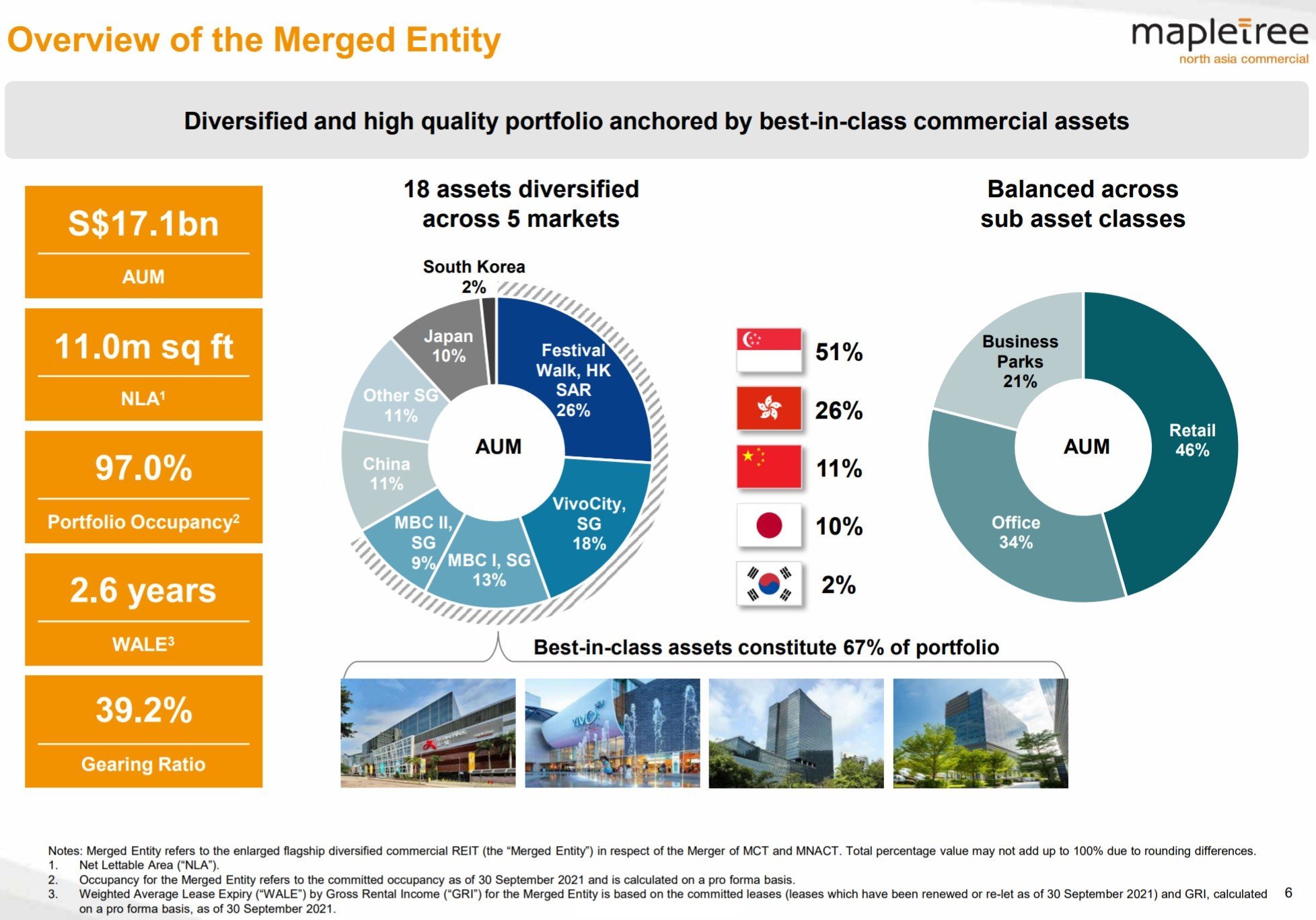

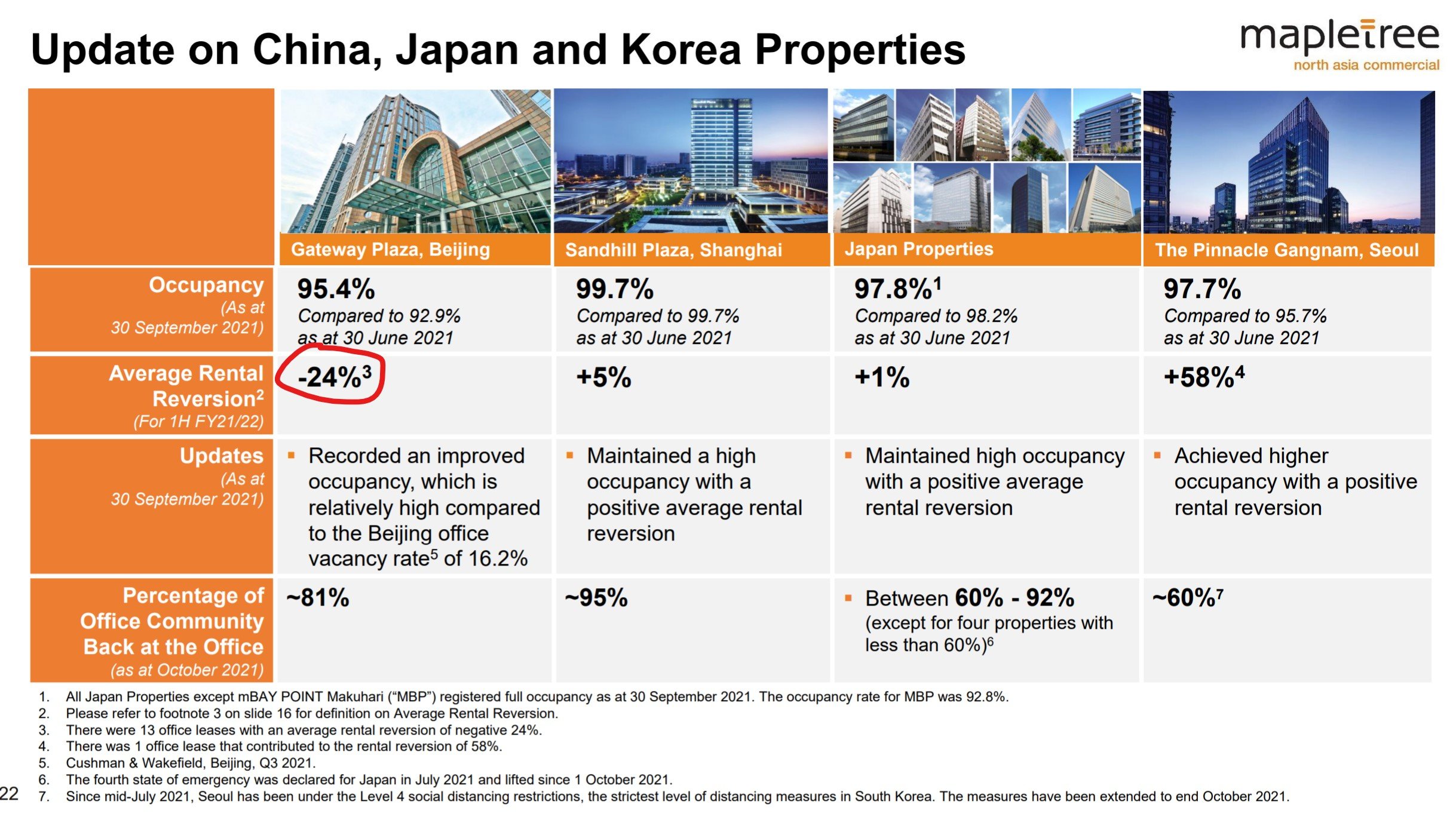

The 2 biggest properties in Mapletree North Asia Commercial Trust are:

- Festival Walk (Hong Kong Mall)

- Gateway Plaza (Beijing Office)

They will form 26% and 7.9% of the newly merged Mapletree Commercial Trust respectively.

I’ve been reading a lot of commentary online, and a lot of investors detest these 2 properties.

The argument basically boils down to 3 factors:

- Only 25 years left on the Lease

- Capitalisation Rate too high

- Rental Reversion is a disaster

Let’s discuss each of them.

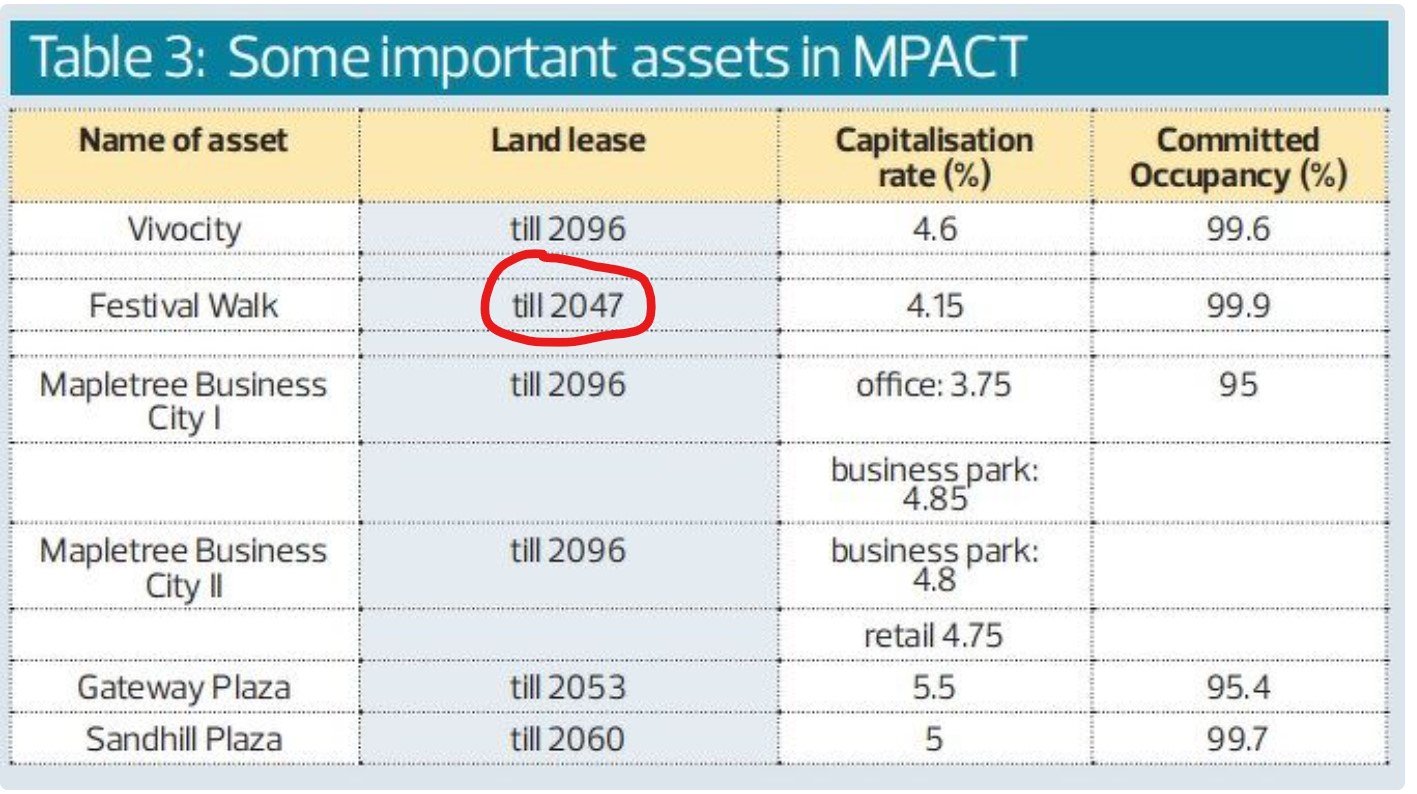

Only 25 years left on the lease (Festival Walk)

A lot of investors have picked up on the fact that Festival Walk’s lease is only until 2047, which is only 25 years left.

Frankly speaking, this was the one I was least concerned about.

SCMP reports:

“According to the policy statement promulgated in July 1997, leases not containing a right of renewal may be extended for a term of 50 years without the payment of additional premiums. Moreover, an annual rent equivalent to 3 per cent of the rateable value of these properties shall be imposed. The case of Pok Fu Lam Gardens extending its lease in 2006 for 50 years without the payment of an additional premium has always been quoted by the government as a possible arrangement for the upcoming expiries.

Lands Department will generally accept applications for lease extensions from relevant owners three years before an expiry date. With the next batch of leases expiring in 2025, the department will only start accepting extension applications for these leases next year.”

So basically, it seems that *most likely* you just pay a small fee, and the lease will be extended for another 50 years.

Mainland China has a similar practice as well. Most of their commercial properties only have a 40-50 year lease, but apparently on expiry on expiry, you just pay a nominal fee to get it extended.

You can argue that the government can always change their mind overnight. It’s not impossible.

But practically speaking, that will unleash a shockwave through the Hong Kong commercial real estate market. Think about what would happen to the other players like Link REIT or Hang Lung. Or the Hong Kong tycoons.

I find the chances of this happening slim at best.

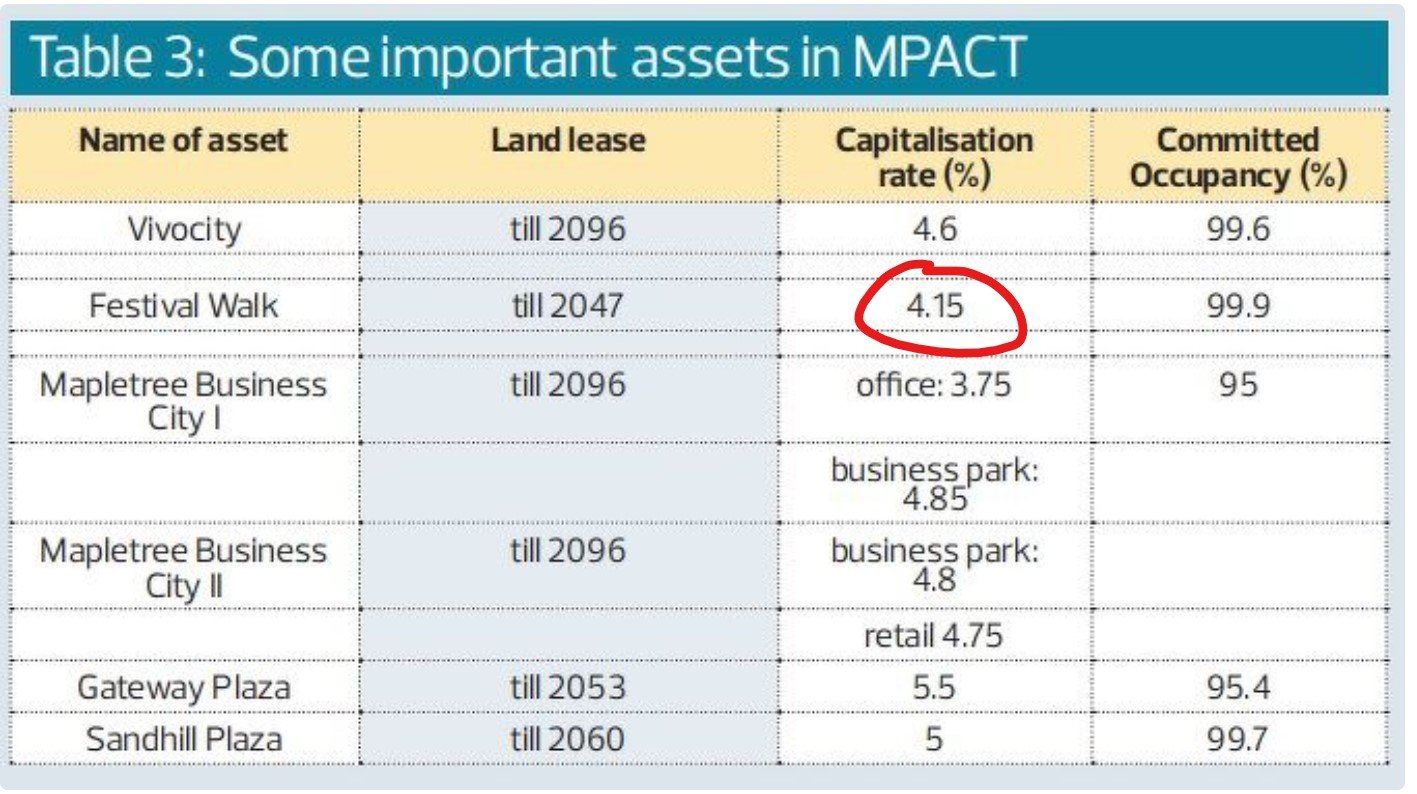

Capitalisation Rate too high

For those newer to real estate, capitalisation rate is basically (Rental Income / Property Value).

The lower the number, the more highly valued it is.

A lot of investors have picked up on the 4.15% capitalisation rate for Festival Walk.

This values Festival Walk as more expensive than Vivocity at 4.6%, which is a far superior mall.

I get it, and I agree with this as well.

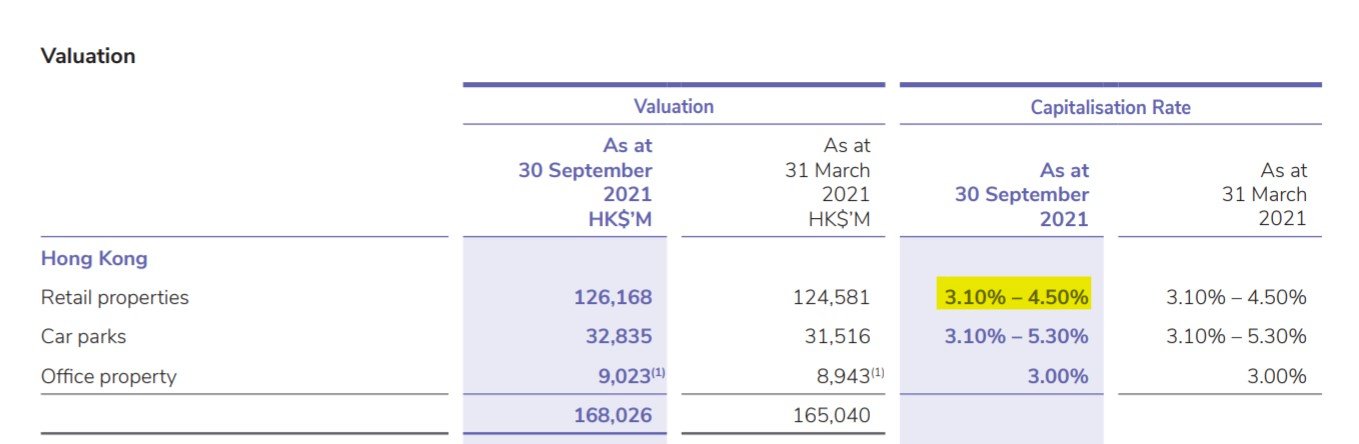

But to be fair to MNACT, Hong Kong is an expensive market.

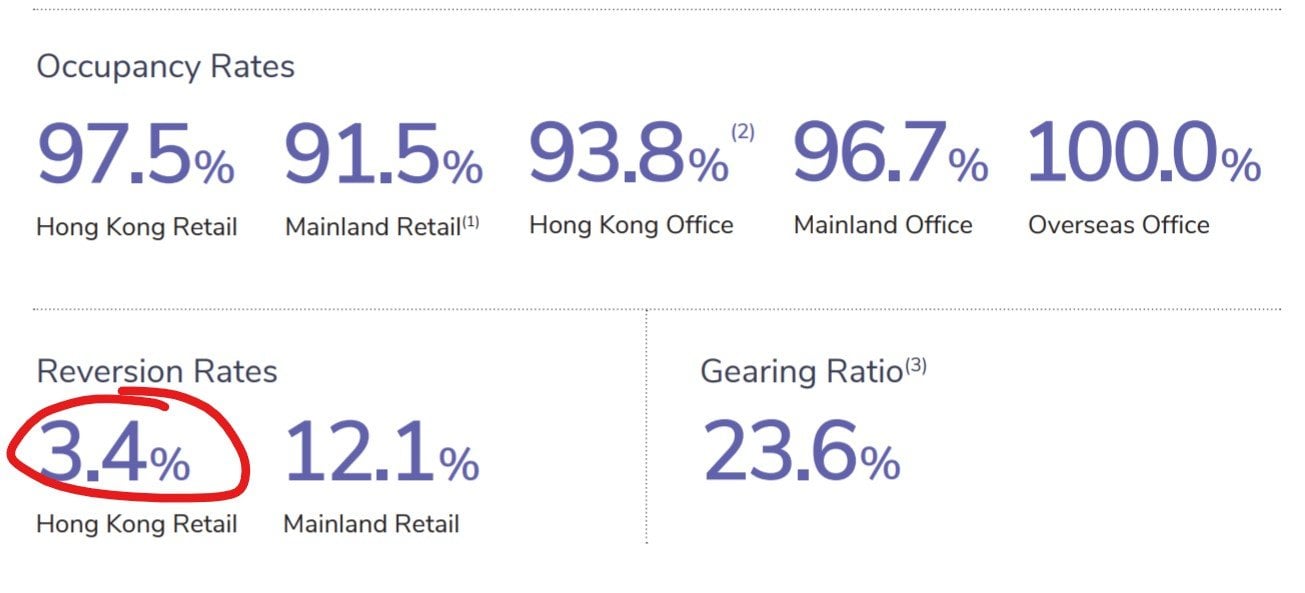

If you take a look at the capitalisation rates for Link REIT (the mega HK retail REIT), you find that their Hong Kong malls are valued at 3.1% to 4.5%.

So Festival Walk is still within this range, and it’s hard to say that it’s grossly overvalued.

If you want to buy a mall in Hong Kong now, this is the price you have to pay.

Rental Reversion

And now for the most frightening point.

Rental Reversions are basically the rent at which a new lease is signed at, compared to the previous lease.

Rental Reversion is a mind blowing negative 30% for Festival Walk, and negative 24% for Gateway Plaza.

I mean… holy shit?!

You’re telling me 34% of the newly merged MPACT has leases being renewed at 24-30% below the expiring lease?

That’s just an absolute disaster.

You can compare that to Link REIT, which has 3.4% rental reversion for Hong Kong retail.

So you can’t even argue that it’s a Hong Kong wide problems. This is unique to Festival Walk.

To be fair to Mapletree North Asia Commercial Trust though, Festival Walk has just been through a chain of disasters.

In 2019 it was trashed by the Hong Kong protesters, that took the property offline for quite a while.

And just this week, there was a COVID cluster at Festival Walk.

Is this mall cursed or what?

Now I love Vivocity and Mapletree Business City, but at this point they only make up 40% of MPACT.

A whopping 34% goes into Festival Walk and Gateway Plaza, which are looking a bit worrying.

Macro Situation in Hong Kong / China

The management insights provide a bit more colour.

To summarise, they expect:

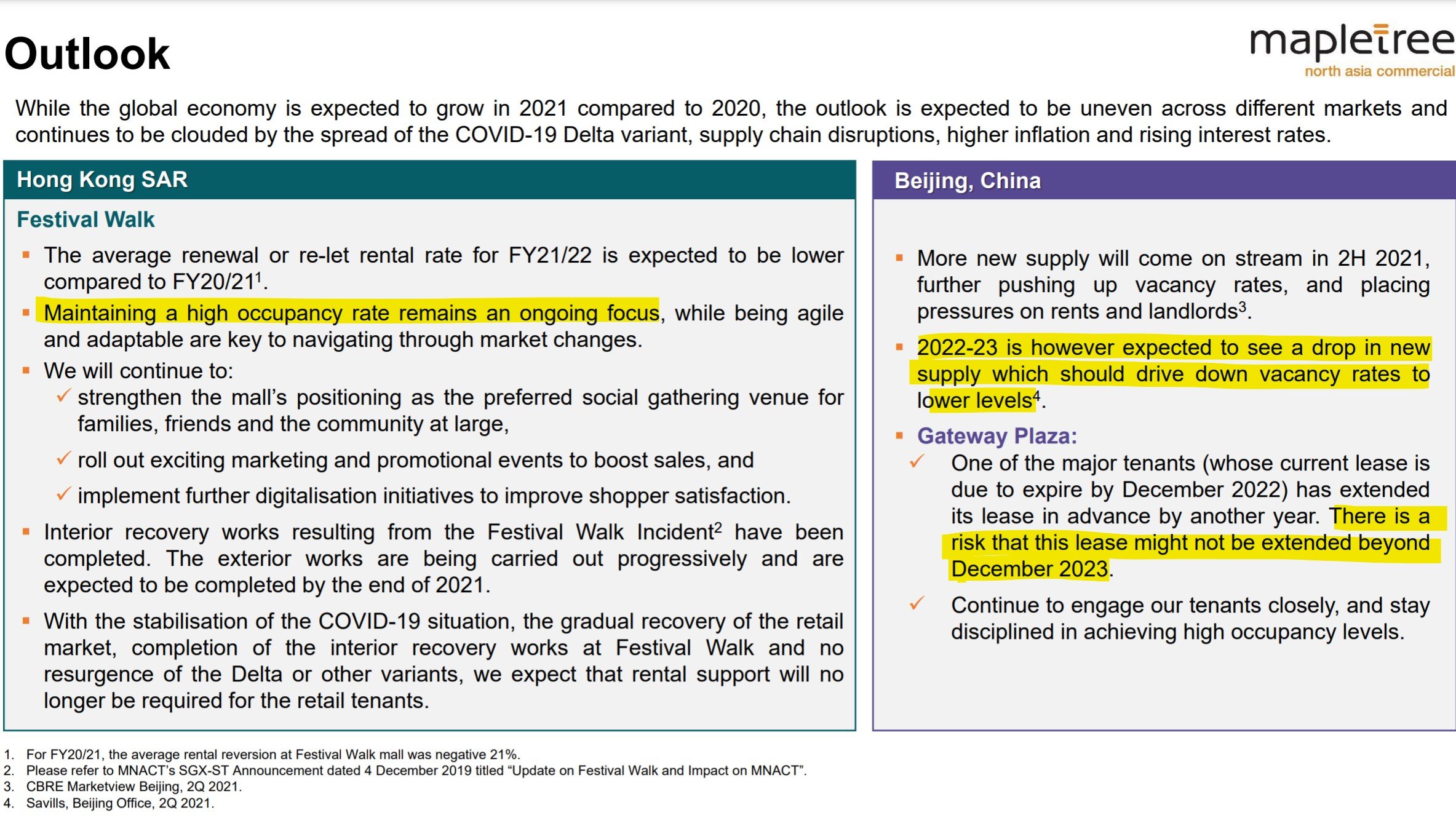

- Rental Reversions for Festival Walk and Gateway Plaza to be poor for the rest of FY21/22

- One of the major tenants at Gateway Plaza has extended their lease to December 2023, and may not extend it further after that

They do explain that the poor rental reversions at Festival Walk is because of them trying to maintain a high occupancy.

Which okay, I can give them the benefit of the doubt.

Management does expect things to pick up in 2022 – 2023.

But I’m just going to take that with a huge pinch of salt looking at the broader macro.

The real estate crisis in China is still playing out like a slow motion train wreck. The tech crackdown is still playing out.

All while China/Hong Kong attempts to maintain zero COVID policy, in the face of the more contagious Omicron.

Whichever way you look at it, I find it hard to get excited about China / Hong Kong real estate short term.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

2. Valuations of Mapletree Commercial Trust

But at this point the sharp-eyed reader will say – Hey FH, there’s no such thing as bad real estate, only a bad price.

And I agree.

As much as Festival Walk and Gateway Plaza are an unmitigated disaster, perhaps the question is – What price would I be a buyer?

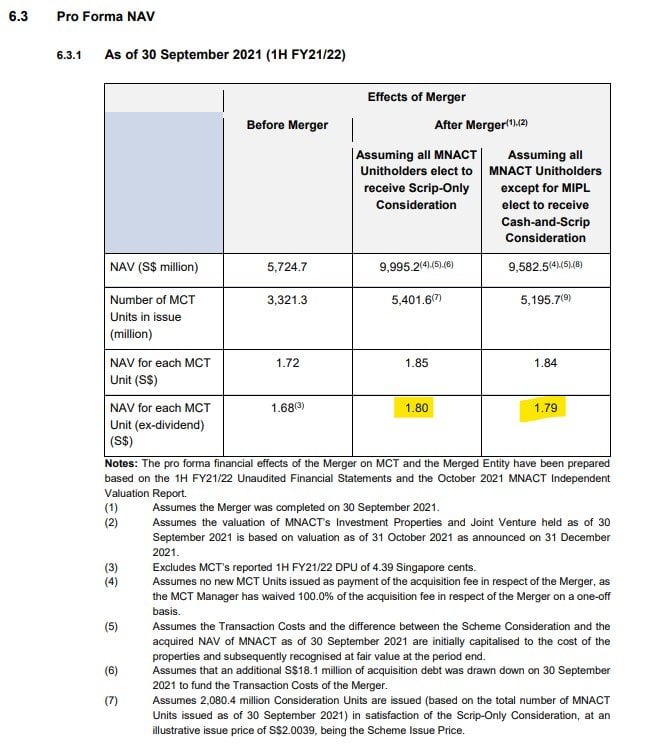

MNACT has traded the past 2 years at about the 0.9+ range, which is about 20% discount to NAV.

And the more I think about it, the more I think that’s the price I would be a buyer of MNACT.

Best case, you could probably convince me to pay up to 15% discount to NAV.

Whereas for MCT I am happy to buy it at a 15% premium to book (1.93 pre-merger).

This is Mapletree Business City and Vivocity after all, the crown jewels of the Mapletree portfolio.

So if you blend them together, you get a range of 0.975 – 1.0x NAV.

Ie. my fair value for the new Mapletree Commercial Trust is $1.74 – 1.79

Whereas MCT at the current price of $1.84 is roughly equivalent to buying the old MCT at 20% premium and MNACT at 15% discount.

I mean that’s ok, but it’s not exactly a screaming value buy if you get what I mean.

I like the CapitaLand REITs more at these valuations

Some comparisons:

- CapitaLand China Trust – trades at 0.73x book value, 6.7% yield

- CapitaLand Integrated Commercial Trust – trades at 0.98x book value, 5.4% yield

Versus MCT at 5.2% yield, 1.02x book value (post-merger).

Which means I can buy CapitaLand Integrated Commercial Trust and CapitaLand China Trust in an 80:20 mix, and get a 5.66% yield.

Higher than MCT at its 5.2% yield, with the following asset allocation:

I get that it’s not an apples-to-apples comparison, but I’m liking the CapitaLand REITs a lot more at these valuations.

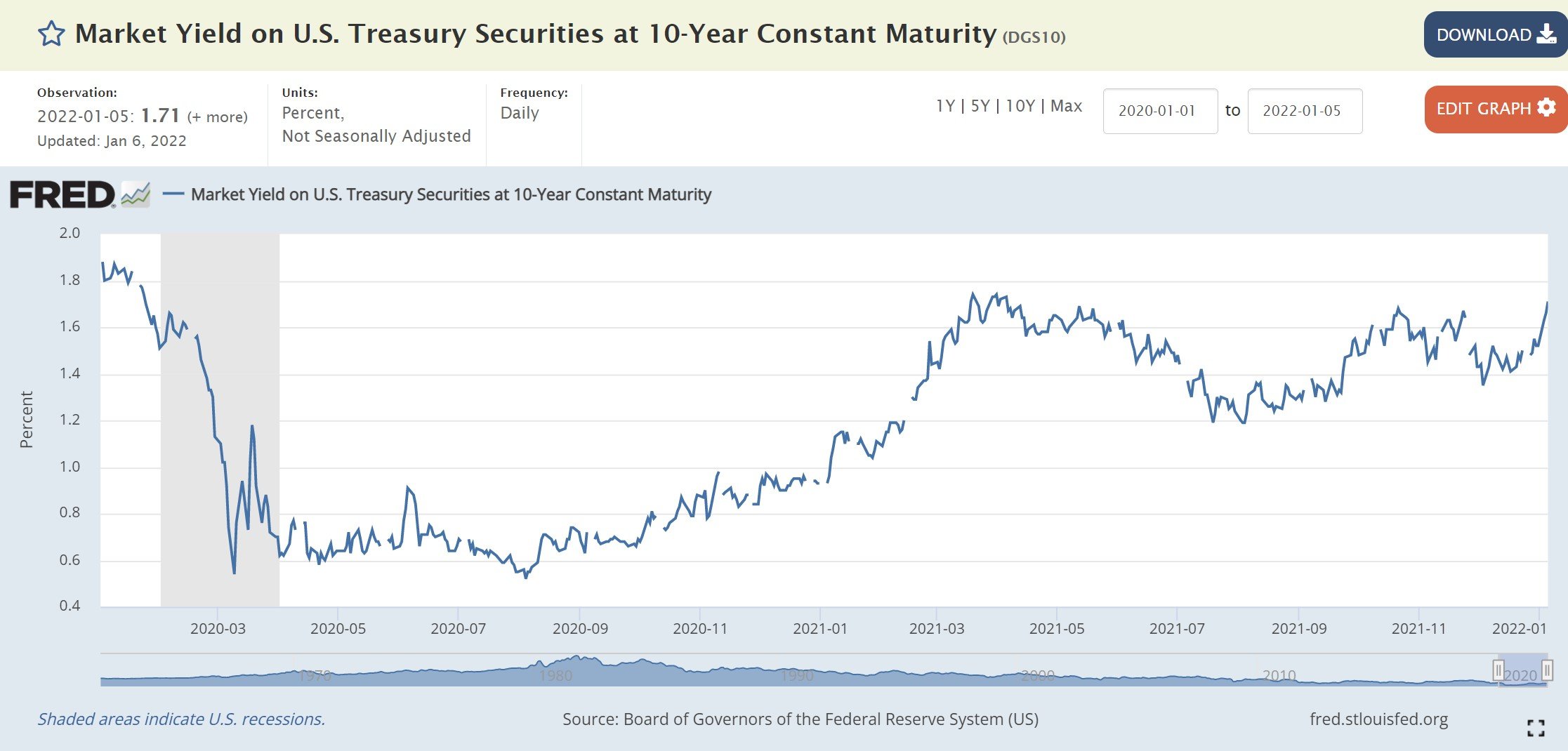

3. Macro Headwinds

In my latest Macro Post, I shared my concerns about rising rates and inflation in 2022.

QE will end by March, 3 rate hikes this year, and now the Feds are talking about balance sheet run off.

It’s important to understand when the macro paradigm has shifted, and I think it very clearly will shift this year (if not already).

The Feds are no longer your best friend, but your worst enemy.

It doesn’t necessarily mean I’m going to sell all my REITs tomorrow, but it also means I will be a lot more selective about the deployment of capital.

I think there will come a time in Q2 / Q3 this year when I will back up the truck and load up on REITs. When everyone is freaking out about inflation and rate hikes.

But I don’t think this is the time just yet.

I haven’t seen capitulation in the bond market yet.

For those who are keen, you can keep track of when and what I buy, together with my full portfolio and REIT / Stock watchlist, on Patreon.

Bonus Point – Technical Damage

By Tuesday alone, Mapletree Commercial Trust had broken through its 50 and 200-day moving averages

You can argue there is some weak support at the 1.8+ level, so that might be an important level to watch.

Whatever the case, the charts are a disaster, and it looks like this may take some time to play out.

There’s a lot of disgruntled MNACT / MCT unitholders who may exit in the coming months, which could place a lot of selling pressure on Mapletree Commercial Trust.

Big Caveat: I am an existing Mapletree Commercial Trust / Mapletree North Asia Commercial Trust unitholder

That being said, I do want to qualify that I already have a big position in MCT, and a smaller position in MNACT.

In fact my average buy in price for MCT is about $1.5.

So my comment that I am not averaging in at $1.84, needs to be viewed in light of all this.

I am already vested in both REITs, it’s just that I am not averaging in at this price.

If you have no position in MCT at all, then maybe the analysis will be different for you.

Closing Thoughts: Is Mapletree still an S Tier Sponsor?

There used to be a time when Mapletree was an S Tier sponsor in my books.

This placed it even higher than CapitaLand and Frasers.

But the recent moves from Mapletree have really led me to question that.

A few months back they dumped a billion worth of China logistics real estate into Mapletree Logistics Trust. Right in the midst of the China real estate slowdown.

And now they’re divesting MNACT into MCT.

And I can’t really figure out why this sudden change of heart too.

Not naming names, but for some of the other REITs where the Sponsor needs cash, or where the Sponsor is publicly listed with its own shareholders to answer to, I can see why they would abuse the REIT.

But Mapletree is a 100% Temasek owned entity. Not public listed.

Who is the one calling the shots, and making these big picture moves? Will there be more to come?

Whatever the case, I’m going to be a lot more cautious on Mapletree REITs going forward.

Love to hear what you think! Are you buying MCT at $1.84?

As always, this article is written on 7 Jan 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Perhaps i should wait until everything is settled before buying the newly listed MCT (with or without MNAT)? Safer?

There won’t be a separate listing, MCT will simply buy out MNACT and rename into MPACT. So if you hold MCT/MNACT now you will simply get shares in MCT after this.

That said, personally for me I would wait for the price to settle down, and/or for it to hit the 1.7+ range before I average in (if at all). But I do have a big position in MCT and MNACT, so what works for me may not work so well for other investors.

Hi FH,

Thanks for the great article once again. For MLT, actually MIP has been developing the warehouses in the past few years. So its not surprising the Sponsor transferred the assets to the Reit? Nonetheless, agree that the MCT merger is a disaster. You guys should vote no.

Regards,

Gerald

https://sgwealthbuilder.com

Yeah it’s not surprising, but the timing was uncanny given China’s slowdown. Could just be an innocent coincidence… but who knows

Hi FH.

I have a big position in MNACT below 0.9. Don’t really care about price appreciation like most of you because the dividend yield has been great for many years which makes my cost low.

What is your opinion for my situation? Sell, Hold, or any other strategy? I’m really confused. 🙁

Please don’t be misled by MNACT’s yield. According to data from Morningstar Inc, payout ratio is 1,012.30%. That means they are eroding capital reserves to please unitholders with high yield while their earnings don’t really justify such payment. Track record: terrible P/E at 168 with unstable income. If not “forced to bail out” MNACT, why should existing MCT unitholders agree to acquire MNACT? Acquisition is tantamount to investment. Will any sane investor consider to buy shares in such a company?

Hi FH,

Appreciate the review.

As a MTnac holder, i’m looking for a replacement stock (undervalue & ~6% yield)

Any recommendation you can think of (can be Reit or non-Reit), preferable SGD denominated.

I’m in for the long term, so holding periods is easily >10yrs.

Thanks

Great question.

There’s no REIT out there at 6% yield with the same risk profile as MNACT, which is one reason why so many unitholders are upset.

CLCT can be looked at, but it’s mainland China so the risk profile is very different.

If it were me trying to replace MNACT I would probably do a combination of MCT:CICT:CLCT and weight accordingly based on risk appetite.

Hi FH,

From your article, I think I will stay away from both Reit, unless there is deep discount. There other good reit out there. To consider.

Since your mention CapitaLand Integrated Commercial Trust and CapitaLand China Trust, would you consider to an analysis for the 2 for us? This could help us understand this 2 reit better. Thanks for the article.

Sure, will see if I can do a deeper dive into the 2 REITs.

Thanks, looking forward to it. Have a nice weekend.

Thank you. I have a small position in MCT and no have time to investigate real-estate scattered throughout Asia. Generally I dislike offices and discretionary retail.

I am more pessimistic than you: Falling DPU may lead to a vicious cycle where the REIT can no longer raise capital to make accretive acquisitions. So not always a case of “if the price falls enough, I’ll buy.”

I know what to do with my shares now.

Haha 50% of the REIT is still the old MCT, so I don’t think it will get to that extent that they can no longer raise capital.

But I agree with you on not wanting to spend time to investigate real estate in other countries. I usually stay away from REITs focussed on US/Europe for this reason.

Hi FH

Thanks once again. Although you pointed out the deficiencies of MNACT, that has been known to most or should be known to most investors

I, for one, was certainly aware of all the double digit rental negative reversions as I accumulated between 96-104 cents all along. The problems associated with their assets and the near term negative view about greater China was very well baked into that price

So, this was not a nasty surprise

However, MCT that traded at significant premium to NAV will and should be expected to trade closer to the post- merger NAV and that will not be unexpected either

But, the ‘discounting difference, now should be valued pro-rata to reflect the ‘fair’ Estimate

This would mean that you weight the premium/discount accordingly as to how much the MNACT and MCT assets will account for proportion wise in the MPACT

I sold off 25% of my MNACT at 1.14 and have started buying MCT- which I had only a small lot before

I will buy more MCT under 1.80 and will sell more MNACT at 1.13/1.14, if at all it gets there to fund this

Overall, REITS with overseas assets including US and EU/UK centric REITS, have not done well in terms of capital appreciation in the SG market. That’s ok as Long as this is compensated by 6-7% plus yields as long as the share price trades within a range. Even then, as I have posted here before, private placements cause problems and you have to buy more post issue to maintain your ‘stake’

Your alternative suggestion of CLCT, which I have held Long term , is significantly down last 1-2 years reflecting the market negativity towards Chinese assets. This is despite their changes mandate etc etc. Although I did add at 1.19, I will add cautiously only lower and slowly

Sasseur REIT did well and yields 8.8% after the unit price peaked at 89/91 c and fell back

In short, all overseas REITS are meant for only distribution gains and that too laced with risks

CICT is good and even then at 2$ and below only

Regards

Garudadri

Thanks Garudadri, this is a fantastic comment.

I actually agree with almost all of your points, nothing much to add for me. I agree with almost all your price targets and outlooks for the REITs as well. Man after my own heart!