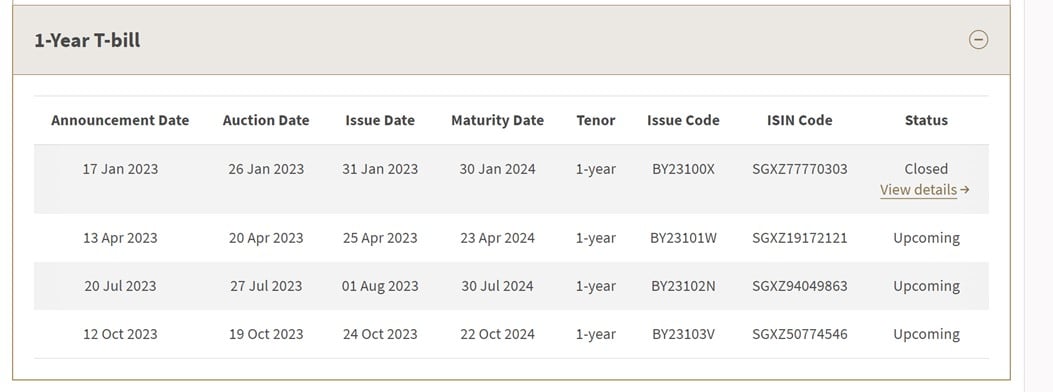

Now there are only 4 12 month T-Bills available for auction in 2023.

And the next one will be available on 20 April 2023.

So those looking to buy T-Bills this month will have the chance of picking between 6 month and 12 month T-Bills.

Given the risk of interest rate cuts over the next 12 months, and given that 12 month T-Bills are trading very close to 6 month T-Bills on the open market.

Should CPF-OA investors switch to buying 12 month T-Bills instead of 6 month T-Bills?

You get to lock in yields for 12 months, and not have to worry about refinancing / rolling over in 6 months time.

In January – I thought that the 6 month T-Bills were a better buy

I looked at the exact same question back in January, and my thinking then was that the 6 month T-Bills were a better buy.

The reason being that back in Jan:

- Those T-Bills were issued at the end of the month, meaning you lost an extra month of CPF-OA interest on maturity

- Good chance of 12 month T-Bills yields coming in low

- Good chance of interest rates being higher or flat in 6 months

A lot of things have changed since January 2023

Well, fast forward 3 months and a lot of things have changed.

Not least a “banking crisis” completely changing the interest rate outlook from the Feds.

Ask me the same question today, and I might say that the 12 month T-Bills are a better buy (if you are using CPF-OA).

Couple of reasons:

- Maturity Date is not the last day of the month

- 12 month T-Bills yields may come in close to the 6 month T-Bills

- Will interest rates be lower in 6 months?

Maturity Date is not the last day of the month

Unlike the January 12 month T-Bills which would mature on 30 Jan 2024 – giving you virtually no time to roll them into new T-Bills or transfer back to CPF-OA.

These 12 month T-Bills will mature on 23 April 2024.

Which means if you are quick about it, you could probably transfer the cash back into CPF-OA before May 2024 – and avoid losing the May 2024 CPF-OA interest.

This alone is a pretty big point in favour of this 12 month T-Bills.

12 month T-Bills yields may come in close to the 6 month T-Bills

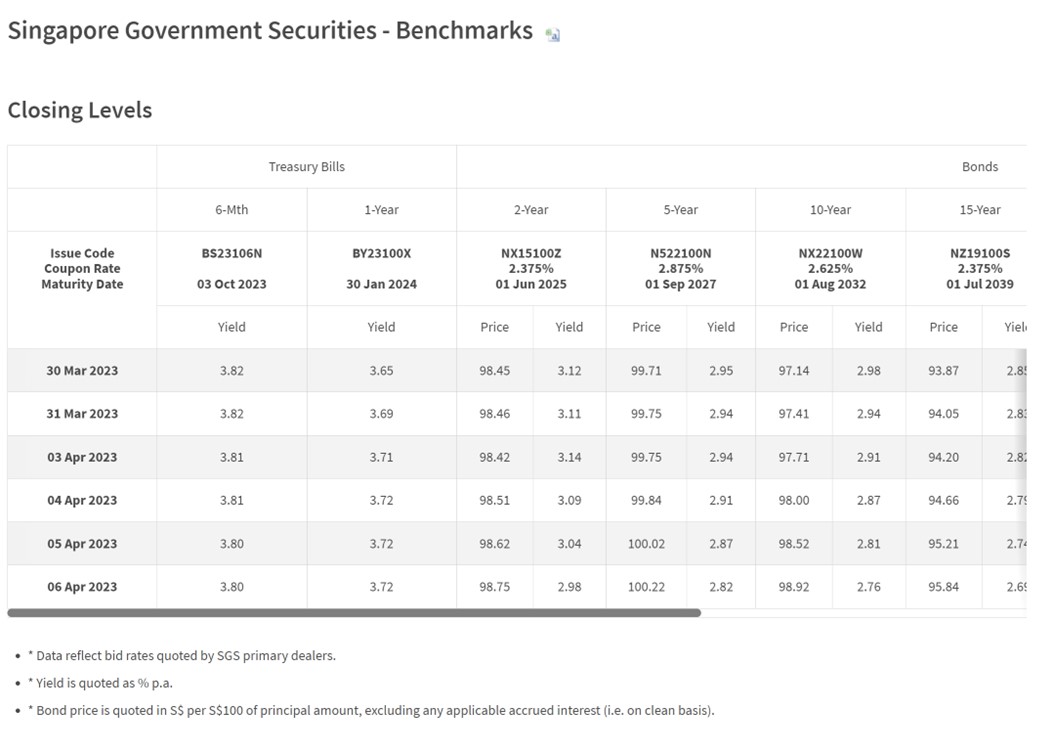

You can also see from market pricing that the 6 and 12 month T-Bills have yields that are quite close to each other.

3.80% on the 6 month T-Bills, 3.72% on the 12 month T-Bills.

Reason being that the market is no longer pricing in significant interest rate hikes (or cuts) in the period falling 6 – 12 months from today.

I think you cannot deny that the interest rate climate has changed completely since January 2023.

Which brings us to the next point.

Will interest rates be lower in 6 months?

In January everyone was still expecting the Feds to hike us to 5.5% and beyond.

So in January, the risk for interest rates was still to the upside.

Whereas today, almost everyone accepts that we’re going to see at most 1 more interest rate hike (if at all).

And after last month’s “banking crisis” – investors are starting to get jittery about when interest rate cuts would start coming into play.

Today, the risk for interest rates is to the downside.

My personal view?

My personal view of course, is that we don’t see interest rate cuts in 2023.

But investing is about risk-reward.

If the 6 month T-Bills trade at 3.80%, and the 12 month T-Bills trade at 3.72%.

And if the interest rate risk over the next 12 months is to the downside rather then upside.

Well – I don’t really see the incentive to buy 6 month T-Bills with CPF over 12 month T-Bills, assuming the auction rates are close to market rates.

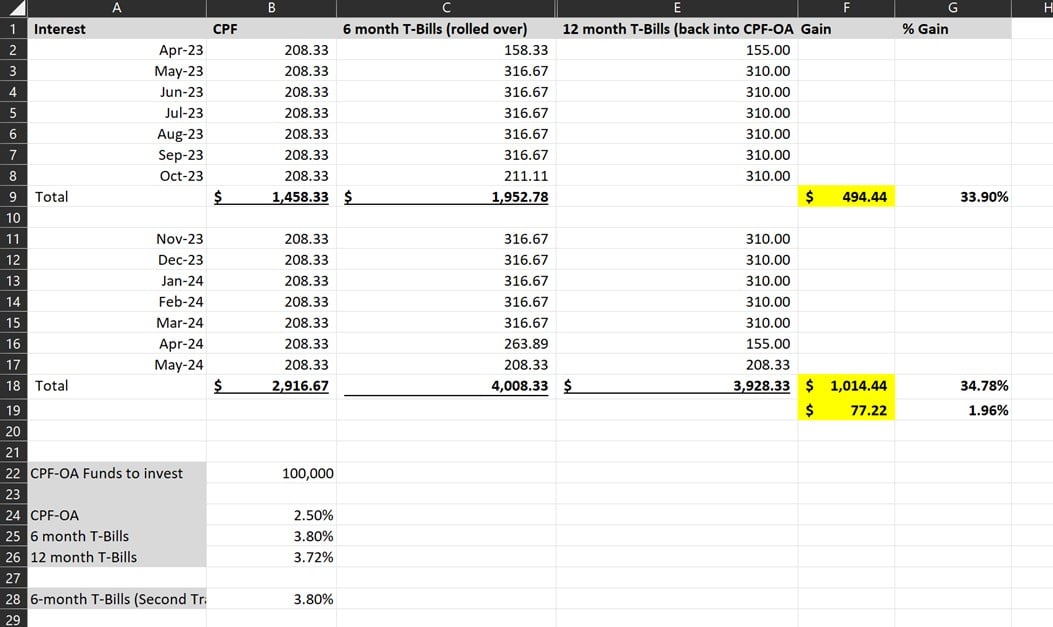

A simple illustration

A simple illustration on this.

Let’s assume the guy who buys 6 month T-Bills:

- Buys them at 3.80% (latest market pricing)

- Rolls them over at 3.80% in 6 months (big assumption here)

- Rolls over the same month (avoids losing another month of CPF-OA interest)

Whereas the guy who buys 12 month T-Bills:

- Buys them at 3.72% (latest market pricing)

Here are the results.

The guy buying 6 month T-Bills makes an extra $77.22 on $100,000.

That’s absolutely tiny, for the amount of additional work and risk.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What is the risk taken on by buying 6 month T-Bills?

Because of course – the biggest assumption we used above…

Is that you can roll over CPF-OA into new T-Bills at 3.80% in 6 months’ time (October 2023).

Is this realistic?

Who knows – market seems to be pricing in an economic breakdown in the second half of 2023.

You can see the difference if we assume the 6 month T-Bills are rolled over at 3.5% – suddenly the 12 month T-Bills come out on top.

Not only that, but the guy buying 6 month T-Bills also needs to scramble to roll over the T-Bills into new T-Bills in October 2023.

Whereas the guy with 12 month T-Bills can just sleep in peace knowing he’s locked in his yields for 12 months, and doesn’t need to lift a finger in 6 months’ time.

What is the risk taken on by buying 12 month T-Bills?

Of course, the 12 months T-Bills approach is not without its risks too.

The biggest one being – whether you’ll be able to buy 12-month T-Bills at close to market pricing of 3.72%.

The previous 12 month T-Bills auction in January was quite hotly subscribed, so the cut-off yields came in quite a bit below market pricing.

This is definitely a risk for the April Auction as well.

Especially if many people have the same thinking as I shared above.

Just a quick note that interest rates are very volatile these days.

That is why I try to write these articles as close to the auction date as I can, to increase the accuracy of the forecast.

So trying to predict the yield on the 20 April 12 month T-Bills today is a bit of a fool’s errand, as a lot of things can change between now and then.

So… this is a big risk to note if you want to go with the 12 month T-Bills.

I leave it up to each investor to decide what is the best course of action.

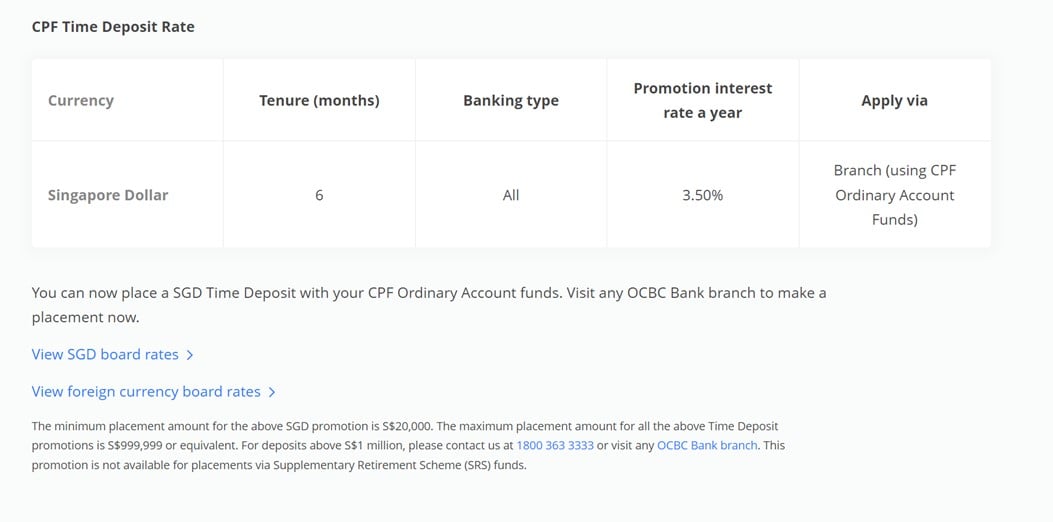

Fixed Deposit not that attractive an option for CPF-OA investors (T-Bills still a better buy)

Just to note that the only Fixed Deposit option available for CPF-OA investors is 3.50% for 6 months with OCBC.

I don’t think this is attractive as it is quite a bit below market yields on T-Bills.

You’re better off just going with T-Bills, especially since the application process is fully online these days.

Timeline to subscribe for the 13 April 6 month T-Bills

In any case, the next 6 month T-Bill Auction is on 13 April.

Those who want to stick with the 6 month T-Bills using CPF should get their applications done by 11 April.

This article is written on 7 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hello FH.

I have a question regarding procedure involved with a T-Bill roll-over using CPF-OA. Suppose a 6 month old T-Bill has matured. I understand that the invested amount will then be returned to the investment account of the bank as there is no automatic transfer back to the CPF-OA account. Then suppose that a new roll-over T-Bill investment is planned for. Can and will the new T-Bill be purchased with the funds which are now in the respective bank’s investment account instead of the account holder’s CPF-OA account? I have a T-Bill maturing soon and if the rates are acceptable, I would like to roll it over but do not know whether I would need fresh funds in my CPF-OA if there are aready sufficient funds in my bank’s investment account. Any clarity on this would be greatly appreciated. Thank you.

Sorry for the delayed reply. Yes – you can use the CPF-IA funds to buy the T-Bills directly. But be sure to use the same agent bank that holds your CPF-IA funds. 🙂

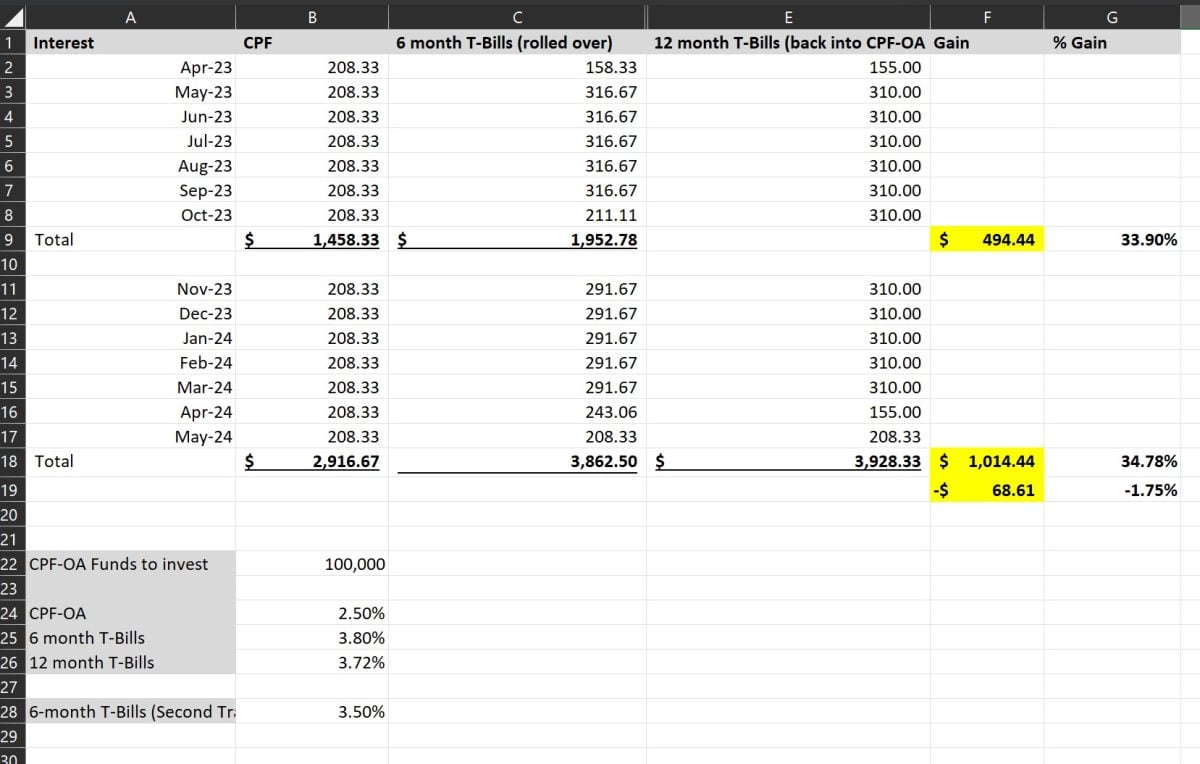

Hi FH, the spreadsheet shows use of CPFIS OA to buy 1-year t-bill maturing in May 2024. There are fees eg CPFIS transaction (and quarterly) fees, which would reduce the $77.22 further for the person who buys 6 month t-bills twice.

Would you take into account that the CPFIS t-bill buyer whose t-bill matures in May 2024 also forgoes CPF interest that would otherwise have been earned in CPF and paid in Jan 2024, if such buyer had kept the $100k in CPF? The investor earns t-bill interest for 1 year, but the opportunity cost is the CPF interest that would otherwise have been paid and compounded year after year.

Yes that is right – I did not account for fees in this set of calculations.

It goes back to how much you are investing – the more you invest, the smaller the fees will be as a proportion of the investment sum. But it does matter at lower amounts.

Yes I have run the calculations for what the investor would have earned had they kept the money in CPF-OA. The calculations are in the first column of the excel shared.

Hi FI, thanks for your reply. CPF interest is credited by 1 Jan of the following year and compounded annually.

If my understanding is correct, CPF interest in Jan 2024 (Cell B13) should be higher than $208.33. The principal in Jan 2024 is more than the original $100,000 as CPF interest was credited. For interest rate to remain a constant $208.33 from Apr 2023 to May 2024 means CPF interest earned in 2023 was not credited by 1 Jan 2024.

If my understanding is correct, which month a t-bill matures makes a difference in terms of CPF interest opportunity cost. For example, consider two t-bills A and B. Assume both t-bills have identical investment amount of $X, identical interest rate, identical interest earned of $Y and identical duration (6 months). The difference is, T-bill A matures in Oct 2023 and t-bill B in Mar 2024.

T-bill A has a lower opportunity cost in terms of CPF interest than B:

A matures in Oct, so both principal and interest is calculated for Nov-Dec and credited by 1 Jan 2024. The CPF interest calculation from 1 Jan 2024 is based on $X+Y.

B matures in Mar 2024. CPF interest on $X+Y starts from Apr 2024, ie later compared to A.

In practice, that means that for t-bill B, $X must be worthwhile to compensate for the non-crediting of CPF interest in Jan.

T-Bills pay the interest upfront though, so you do need to factor that in as well.

I get what you mean on opportunity cost though.

It’s a fair point, and worth considering.