It’s funny because I actually wrote this article a few weeks back before the new round of cooling measures.

But then the cooling measures came out this week, and the topic of how to get around ABSD would take on renewed importance.

So I figured I would release this guide, which is Part III of the FH Property Series (see Part I – How to Pick Property and Part II – How to Price Property).

How to avoid the dreaded ABSD when buying a Singapore property.

How should you structure your legal holdings, how to hold your property, and how to decouple your property to avoid ABSD.

Let’s go!

Huge Christmas Promo for Investing MasterClasses!

Sign up now and get massive discounts and limited Freebies!

Find out more here.

Basics: Joint Tenancy or Tenancy in Common

A bit of basics to frame the discussion. For those familiar with legal structures and taxes feel free to skip this section.

There are 2 ways you can hold a property in Singapore:

- Joint Tenancy

- Tenancy in Common

Joint Tenancy is the default option.

Each person holds equal stakes in the property, and when one dies the other person automatically gets his/her stake (right of survivorship for the lawyers).

If you buy with your spouse, this is the default option unless you know what you’re doing.

Tenancy in Common is more for commercial transactions.

The main difference is that Tenancy in Common allows you to define the ownership stake for each party.

So Person A may hold 10% ownership, and Person B may hold 90% ownership.

When you buy the house just tell your lawyer what you want, and they will handle the paperwork for you. You can also get them to answer you on the pros and cons.

Taxes / Stamp Duty when buying a property in Singapore

3 big taxes to take note of when buying a property in Singapore:

- Buyer’s Stamp Duty (BSD)

- Additional Buyer’s Stamp Duty (ABSD)

- Seller’s Stamp Duty (SSD)

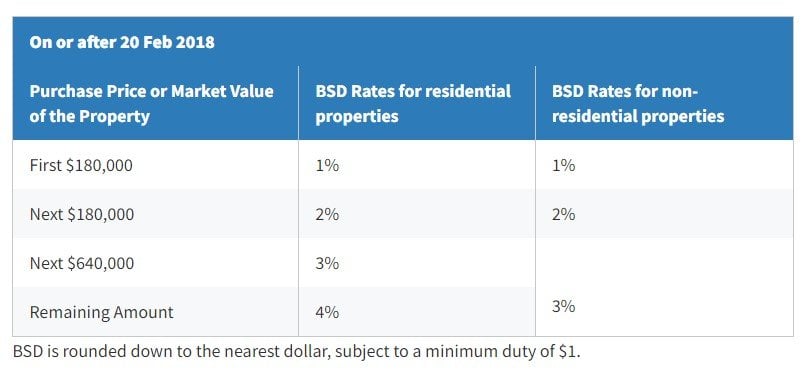

Buyer’s Stamp Duty (BSD)

Buyer’s Stamp Duty is the plain vanilla stamp duty, paid when you buy a property in Singapore.

There’s no way around this, you just have to pay it.

Additional Buyer’s Stamp Duty (ABSD)

Additional Buyer’s Stamp Duty (ABSD) is the stamp duty when you are buying a second home.

This was what the goverment increased in the cooling measures announced this week (latest rates below).

There are ways to get around it if you plan ahead, that we’ll discuss in today’s article.

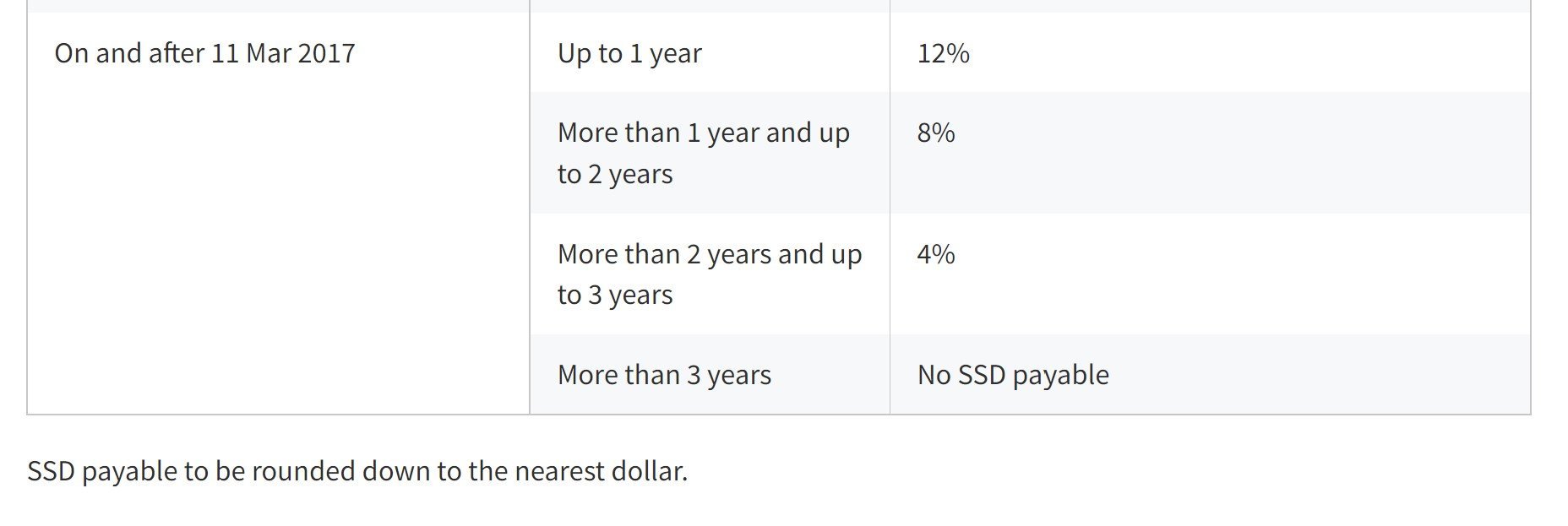

Seller’s Stamp Duty (SSD)

Both ABSD and Seller’s Stamp Duty (SSD) were introduced more recently to curb speculation in property.

Seller’s Stamp Duty triggers when you sell a property within 3 years after buying it, and you can see the rates below.

Stamp Duty triggers when the OTP is exercised, not on completion – for ABSD, BSD and SSD

The important thing to note is that Stamp Duty triggers when you exercise the Option to Purchase (OTP), and not on completion.

Once you sign the OTP and exercise it (after you pay the 1% deposit and 4% exercise fee), then you need to pay stamp duty to IRAS within 14 days.

Likewise, if you already signed an OTP to sell your house and the OTP has been exercised, then that property does not count for ABSD rules.

The reason why is because legally, the proprietary interest in land moves on exercise of OTP, and from that point on completion is specifically enforceable. So you already own the equitable interest in the land.

But that’s just lawyer speak, all you need to know is stamp duty is tied to option exercise.

How to avoid paying ABSD when buying a private property in Singapore? (Assuming first property is Private)

I’ve set out the ways to avoid ABSD below, ranked from easy to complex.

Easy ways to avoid ABSD

- Decouple

- Buy in 1 spouse’s name

Medium ways to avoid ABSD

- Sell one, buy two

Complex ways to avoid ABSD

- Hold 1% for easy decoupling

- Put in children’s name

Other ways to avoid ABSD

- Buy EC

- Buy commercial property

Let’s run through each of them.

FYI I’m writing this guide from the perspective of a married couple (with / without kids), which I assume is the majority of buyers trying to avoid ABSD.

If you’re a single buyer, the concept here still holds, but you need to get more creative in the implementation.

This part of the guide assumes your first property is a private property. We’ll discuss the scenario where your first property is a HDB / BTO in the next section below.

Please do not take this article as legal advice. If you are in doubt as to the course of action you should take, please discuss with your lawyer or tax advisor before you proceed as there may be additional intricacies for your personal situation.

Easy – Decouple the Property

The concept is simple:

- Husband and wife own a property as joint tenants.

- Husband sells his stake to wife (or vice versa).

- Husband now owns no property – and goes on to buy a new property without ABSD (or vice versa)

You need to engage a lawyer to decouple the property for you, and the main fees to take note of are:

- Legal Fees

- Buyer’s Stamp Duty

- Loan Refinancing

- Seller’s Stamp Duty

Legal Fees

Decoupling is more complex than the average conveyancing because you need a lawyer for both the buyer/seller.

Expect to pay about $5,000 to $7,000 in legal fees.

Buyer’s Stamp Duty

This is payable on the value of the interest in the property being sold.

So if the house is worth $1 million, and Husband sells his 50% stake to his wife, then Buyer’s stamp duty is payable on $500,000 and not $1 million.

IRAS takes the higher of (1) amount paid or (2) market value, so don’t think that you can put purchase price at $1 to fool IRAS.

Loan Refinancing

Because Husband is selling his stake entirely, he needs to pay off the mortgage, and there might be break fees on the mortgage (usually 1% of mortgage amount).

I would suggest to time your decoupling together with the end of your mortgage lock-in period, to avoid paying this fee.

Bonus Tip – If you refinance your loan at the same time as the decoupling, the new bank usually gives you a legal subsidy of about $2,000 that you can use to offset decoupling legal fees.

Do note that because you are refinancing, both spouse needs the income to service the mortgage under the TDSR rules. There are ways around this via show funds, which we’ll discuss further under the loan financing part of this FH Property Series.

Seller’s Stamp Duty

If you’re decoupling within 3 years, you also need to pay Seller’s Stamp Duty.

Sometimes decoupling costs more than ABSD

Remember to do the numbers before you decouple.

Sometimes if you need to pay the break fee to your bank and seller’s stamp duty, the total fees may actually be higher than the 17% ABSD on your new property (especially if the new one is cheap).

In such cases don’t decouple!

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Easy – Buy in 1 Spouse’s Name

Of course, if you plan a bit ahead, and you know that you want to buy a second property down the road, you can save yourself on a lot of hassle and fees by just putting the first property in 1 spouse’s name.

But reality is a bit more nuanced, and most people don’t (or can’t) do this because:

Mortgage Servicing Ratio – One spouse’s income is not sufficient to service the full mortgage amount (although you can show funds to increase the mortgage amount)

Trust Issues – Sometimes people just don’t want to be paying for a property that is legally owned by the other spouse. Hey it’s your marriage, I’m not judging.

Change in life circumstances – A lot of times people don’t expect to be buying a second property so soon. But then their income goes up, they have a kid, they change workplaces, and they decide to buy a new property.

That said – if you can plan ahead and solve these 3 issues, buying the property in 1 spouse’s name is probably the easiest way around ABSD.

Medium – Sell one, buy two

With this method, you sell the existing property you own, and you buy back 2 properties, one in each spouse’s name.

I listed this as medium complexity because there are quite a few considerations to take note of.

Don’t use this if your existing property has significant upside potential

If your existing property has significant upside potential that is not recognized by the market, it won’t make sense to do this.

For example your property might be going through an en-bloc, or a new MRT line is coming up in 2 years.

You expect the value of the property to go up to $2 million when that happens, but buyers today are only willing to pay up to $1.5 million.

Be honest with yourself though – who are you trying to kid?

But if this is indeed the case, then it may not make sense to sell your existing property.

Selling 1 property and buying 2 concurrently is not easy to execute

Execution is genuinely hard for this method.

You need to sell 1 property, and buy 2 back concurrently.

You need to find a buyer, while concurrently house hunting for 2 properties to buy back at the same time.

Sure, you can wait for a while before buying back the new property, but if you do that you must understand that you’re effectively taking a position on market timing.

The equivalent is selling all your stocks today and trying to buy back double the amount in 6 months.

If prices go up significantly in the interim, you could lose a lot of the profits you made on your sale.

So sell one, buy two sounds easy in theory, but in practice it is a lot harder to execute than you would imagine.

If your first property is a good one, I don’t recommend doing this unless you really know what you’re doing.

Complex – Hold 1% for easy decoupling

This method can be easy or hard.

That’s because the key point to manage is your relationship with your spouse.

The way this works is very simply– Husband holds 1% as tenant in common, and wife holds 99%. Or vice versa.

When you decouple, you only pay stamp duty on the value of the 1% stake.

The main risk with this approach is your relationship with your spouse.

If you divorce your spouse, legally you only hold 1% of the property, so it will be tricky for you.

That said, a lot of old businessmen do this, so that in a bankruptcy the creditor can only go after their 1% stake in the house.

A lot less popular in today’s society.

Complex – Put in children’s name

This one is also easy or hard depending on your child’s age.

If your child is above the age of 18 and drawing an income, it’s quite straightforward.

You buy the property in your child’s name, and you show funds to the bank to increase your mortgage amount.

The tricky part is when your child wants to BTO or buy a property with their spouse. Then you need to either (1) sell the property or (2) your child pays ABSD on the new property.

If your child is young and below 18 though, it gets very tricky.

You need to use a trust structure to hold the property on trust for your child.

And you may or may not be able to take up a loan from the bank.

IRAS may also view the trust as a sham trust to avoid ABSD – thus charging you full ABSD down the road, so you need to be very, very careful with the legal structure.

If you’re doing this, I would suggest you get a good lawyer. The trust documentation needs to be watertight. Any residual interest or control left to you could trigger ABSD.

And approach the bank early because the mortgage could be tricky.

Others – Buy EC

There are a few other methods which are more of “cheating”, and not really avoiding ABSD.

Buying an EC is one of them.

EC doesn’t count as private property, so no ABSD is payable as long as you sell your existing private property within 6 months.

At the point when the OTP is exercised, you can apply to IRAS for stamp duty remission, and you get a 6 month grace period to sell your property.

Others – Buy Commercial Property

If you buy commercial property like a shophouse or industrial property, those don’t count as long as they are not zoned “Residential” by URA.

So no ABSD is payable.

How to avoid paying ABSD when buying a private property in Singapore? (Assuming first property is BTO / HDB)

Ok so that’s if you own a private property. If you own a HDB, the options are much more limited.

Can you decouple a HDB to avoid ABSD?

The main reason why is because you cannot decouple a HDB if you are a married couple.

Under the rules that took effect in April 2016, transfer of ownership of an HDB flat is only allowed for divorce, marriage, medical reasons, death of an owner, financial hardship and renunciation of Singapore citizenship.

So you cannot sell your HDB / BTO to your spouse, and you cannot have it held in 1 spouse’s name only.

So the only decoupling options are:

- Ex-spouse – but don’t divorce just to avoid ABSD!

- Sell to Family members – after MOP (but your family needs to be able to buy a resale HDB)

Because of that, the only realistic options for a HDB / BTO flat are:

- Sell 1, Buy 2

- Fulfil MOP and Pay ABSD

- HDB Essential Occupier

Sell 1, Buy 2

You sell your HDB, and buy back 2 properties.

The problems with this are similar to what we discussed above.

If your HDB is Pinnacle@Duxton, it will make more sense for you to just pay ABSD. You’ll make it all back via rental in a few years.

Fulfil MOP + Pay ABSD

What most people end up doing, is that they just wait until the 5 year MOP is up, and then they pay ABSD on the condo that they buy.

This is what most people I know end up doing if their first property is a HDB / BTO.

You rent out the HDB at a juicy 6-7% yield, and you live in your fancy condo.

Or you could always rent out the condo at a sad 2-3% yield, but stay in your HDB and blow the extra cash on a brand new Porsche. ????

HDB Essential Occupier

According to HDB, an essential occupier refers to a family member who is part of a family nucleus, which is necessary to qualify for HDB.

This is different from being an owner or co-owner of the flat, as essential occupiers do not have a share of the apartment or any legal right in it.

So while most couples buy the HDB under a joint tenancy, another way is to have it only owned by 1 Spouse, and have the other spouse added as an “essential occupier”.

This way, you fulfil the family nucleus for HDB purposes. But the spouse that is the “essential occupier” does not legally own any property, and will be regarded as a first time buyer.

Do note though that the spouse will still be subject to the 5 year Minimum Occupation Period, and can only buy another property after the 5 years MOP is up.

The downside with this is that because the Essential Occupier Spouse is not a legal owner of the HDB, he/she:

- Cannot use their CPF to pay the mortgage / downpayment

- Cannot use their income to apply the mortgage (the other spouse must fulfil the TDSR requirements by themselves)

- If the spouse that legally owns the HDB passes away, there is no joint tenancy to kick in, and the HDB will be distributed via the will (or go into intestacy if there is no will).

So there are quite a few cons with this approach, and may not be suitable for everyone. Do discuss with your lawyer if in doubt.

Closing Thoughts: Avoiding ABSD when buying Property in Singapore – Right or Wrong?

There’s a difference between tax avoidance, and tax evasion.

Tax avoidance is the methods we discussed above, perfectly legal.

Tax evasion is buying a property and not paying stamp duty, that’s illegal and you go to jail.

You could argue that some of these loopholes need to be fixed, and I don’t disagree.

The government has already taken steps to address the Prime Location Housing HDBs, so we may see further changes to the stamp duty rules in due course.

I’m not here to tell you what the law or policy should be going forward. That’s for parliament to decide what’s best for Singapore.

If they decide to close off these loopholes, perfectly ok by me.

All we can do as investors is to figure out how, based on current rules – how do we avoid paying ABSD when buying a second property in Singapore.

I’ve set out the main ways to avoid ABSD in Singapore based on prevailing rules in 2021, but do note that this may change going forward.

I would love to hear what you think. Are there any other methods to avoid ABSD in Singapore that I missed out?

Huge Christmas Promo for Investing MasterClasses!

Sign up now and get massive discounts and limited Freebies!

Find out more here.

very interesting article.

could you elaborate more on this: “Sell to Family members – after MOP (but your family needs to be able to buy a resale HDB)”

my hdb has already my spouse as essential occupier already.

Basically it’s to sell to another family nucleus. For eg. your parents if they do not already own a property.

Hi, does this mean that I can sell to my part to my in-law after MOP (they hold LTVP) and then I’ll become property free?

Yes if they have a family nuclues this is possible. It is effectively a HDB version of decoupling, and there are stamp duty and legal fees etc incurred.

Buy a soho (commercial title)

Yeah that works. 🙂

For the part on buying an hdb flat with your spouse as essential occupier may not work if you are taking a full family grant. The spouse will be considered as a second-time applicant as the family grant is given to a ‘couple’. Having said that, I am not too sure whether applicant=buyer when considering ABSD. If not same, then it may work.

Yes there are many potential drawbacks with the essential occupier approach. So it really depends on one’s individual circumstances. 🙂

Under essential occupier route, can my wife whose the essential occupier now buy an HDB and list me as an essential occupier after MOP?

Do you mean a new HDB or resale? Resale might be doable, but don’t believe so for new HDB. Just check with your lawyer / HDB before you make any firm decisions.

How about waiting till both (married couple) are 35 to sell current hdb & buy one hdb resale each?

True ya that could work. Assuming MOP is up, and one is buying resale.

Hi FH,

ST came up with an article on how more Singaporeans invest overseas in the wake of tightening measures in SG property. What do you think of that, and which markets would you recommend for wealth preservation and capital appreciation?

Actually investing overseas is quite a complex endeavour. One needs to be familiar with regulatory issues, FX risk, financing risk, and the difficulty in managing a property in which one is not primarily based in. I’ve seen many cases of investors getting burnt where they are not careful.

The rare success stories I know of are from early investors in China, where they rode the secular bull market in the early 2000s. And even then they had to exit by 2010s because of regulatory concerns.

Unless you are familiar with the local market (eg. you grew up there, have a spouse from there), I personally am not a big fan of investing in private property overseas. Better to just buy a REIT and let the professionals handle it for a small fee.

@James

Married couple are considered one entity and not allowed to buy separately under singles scheme. You need to divorce if you are married or marry after 1 person has bought under singles scheme i.e. other party buys private.

@Smudger

If your wife is an essential occupier with you as the owner, she cannot buy another HDB flat. You are also not allowed to be listed as an essential occupier since you already own a HDB flat.

Thank you! Appreciated. 🙂

My understanding is if you are holding a private property you can’t apply for a EC.

Yes that’s right.