Dividend stocks seem to have fallen out of favour recently.

Dividend stocks are less sexy, but they’re still a very important part of any Singaporean portfolio.

I would even go so far as to say they are the bedrock of the portfolio (on which you layer on growth stocks for upside).

So let’s look at the top 5 high dividend stocks to buy in Singapore – in 2021.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list.

Don’t forget to join our Telegram Channel and Instagram (or our Reddit Community)!

[mc4wp_form id=”173″]

Dividend Sustainability vs High Dividend Yield Stock

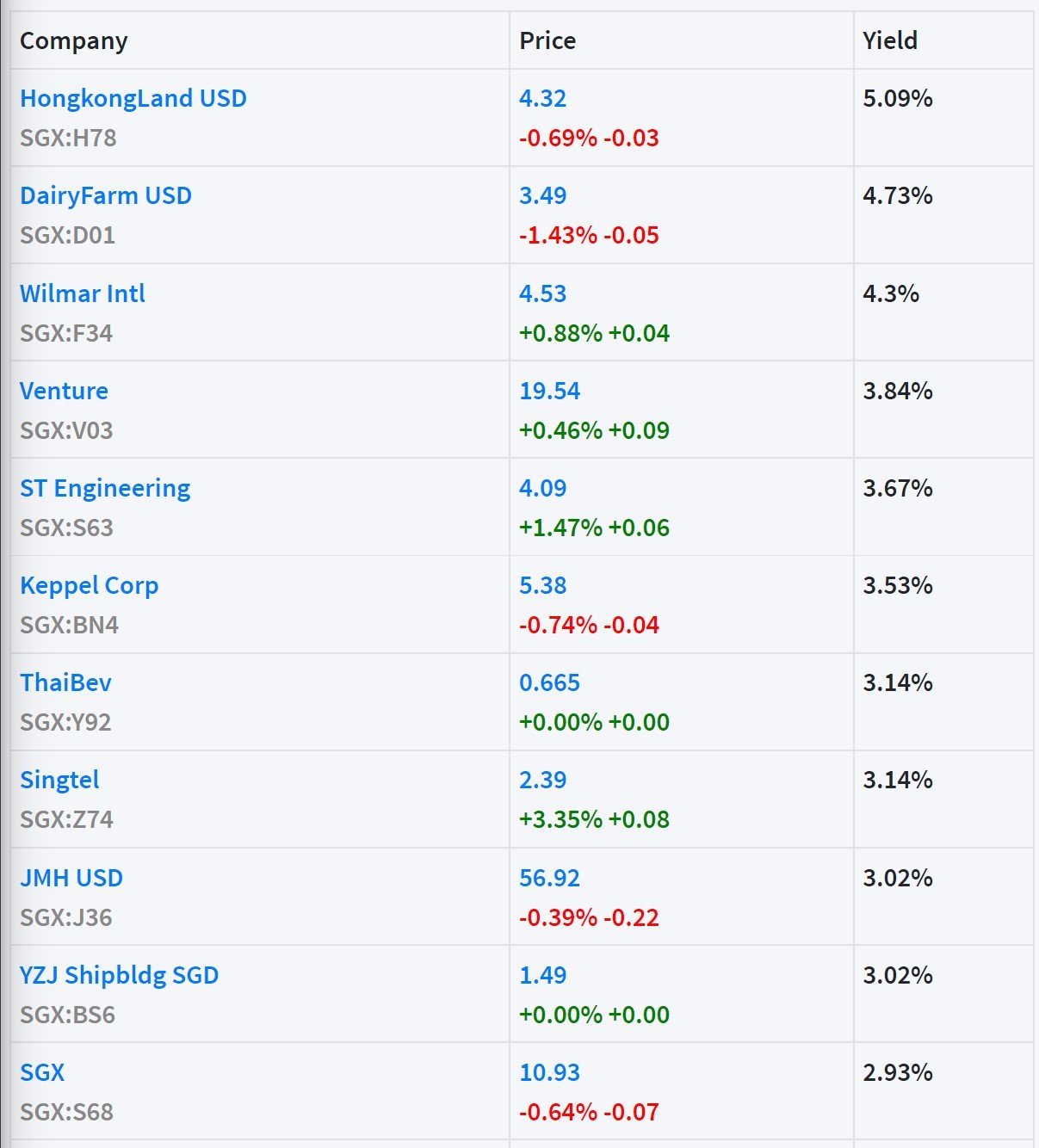

If all you want is a high dividend – I’ve extracted the list of highest yielding blue chip dividend stocks in Singapore below.

But of course, there is more to dividend stocks than just a high dividend.

Think about Starhub – they were trading at a 7% dividend a while back.

But the core business was in decline, and if the business couldn’t generate enough cash to sustain the dividend, eventually the dividend was cut.

The market is efficient in this way – when a stock has too high a dividend, there’s usually a good reason why.

So when evaluating high dividend stocks in Singapore, we’ll focus more on total return – both (1) dividends, and (2) capital gains (or avoiding a capital loss).

We’ll try to find dividend stocks with:

- High dividend yield

- Low dividend payout ratio (the dividends paid out as a percentage of overall profits – low is better)

- Sustainable core business (to sustain the dividends long term)

REITs or no REITs?

I deliberated long and hard about whether to include REITs in this list.

If I did, this list would be easy to come up with, but also way less fun.

So in the end, I decided to exclude REITs from this list of high dividend Singapore stocks to buy.

If you are interested in REITs, you can check out our previous REIT article here.

1. Hongkong Land Holdings Limited (SGX: H78)

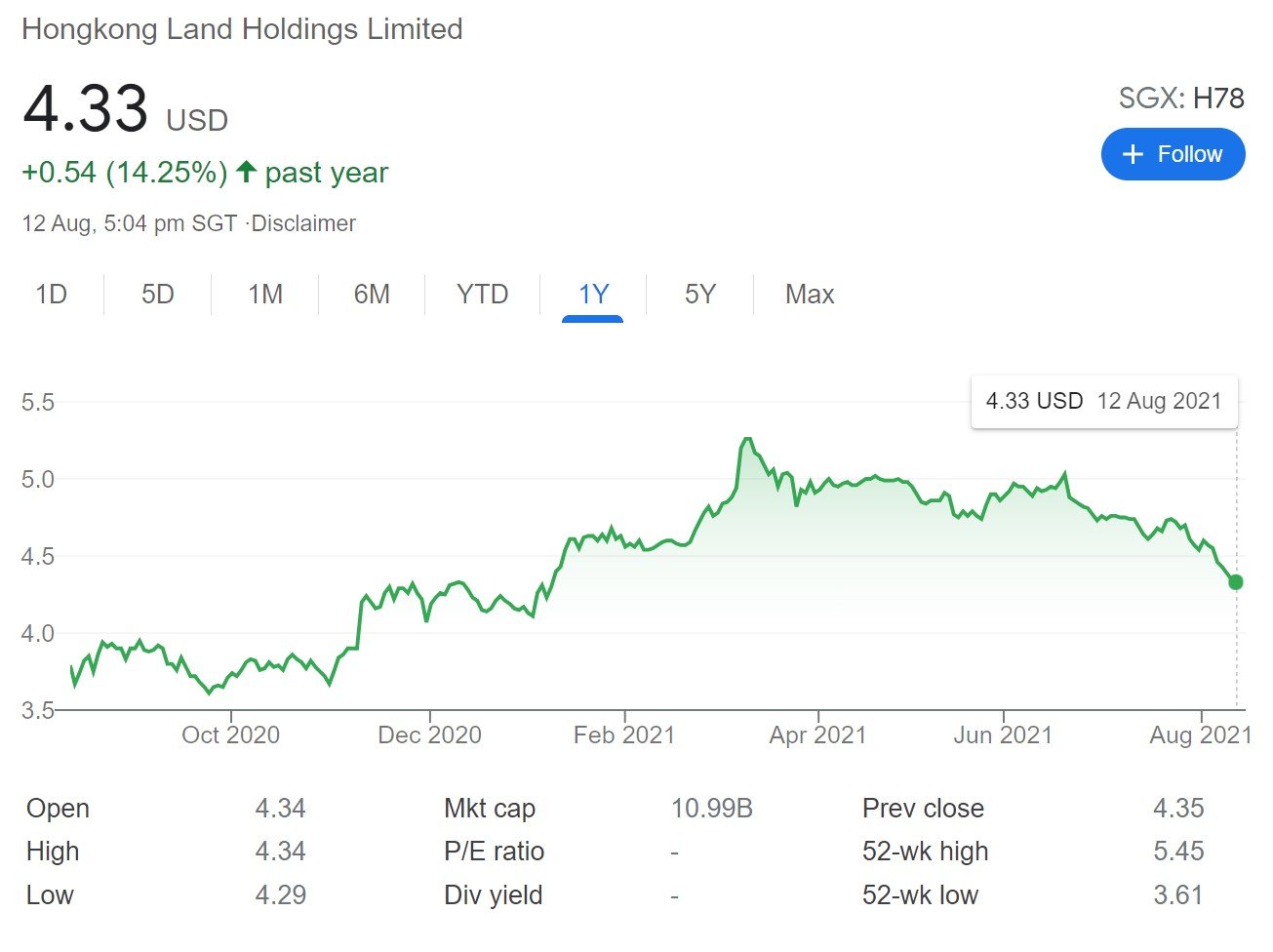

Stock Price: 4.33

Trailing Dividend Yield: 5.09%

Price / Book: 0.29x

Dividend Payout Ratio: 50%

Probably the most controversial dividend stock on this list.

Hong Kong Land.

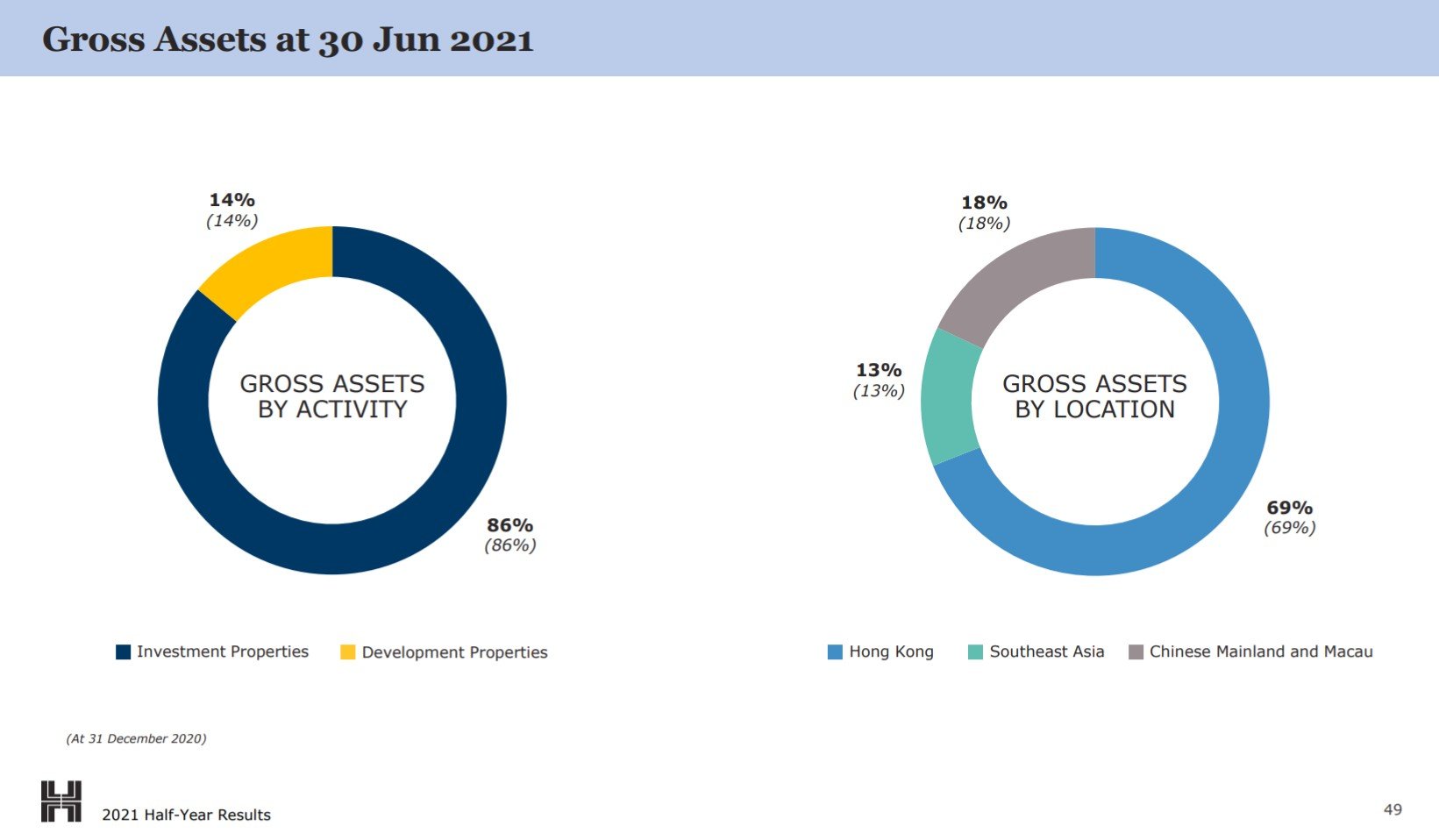

Hong Kong Land is a very old company, that owns real estate across Hong Kong, Singapore, and China.

The bulk of its assets (69%) is located in Hong Kong:

In fact it’s the single largest landlord in Central, Hong Kong.

You can look at the properties owned below, investors familiar with Hong Kong will know the area well.

At today’s price, Hong Kong Land trades at a mind blowing 5.09% yield, and a ridiculous 0.29x book value. That puts many blue chip REITs like MCT and CICT to shame.

Oh and did I mention the dividend payout ratio is only 50%?

But remember how we said the market is pretty efficient – and high yield dividend stocks usually trade at that yield for a reason?

There are 2 big problems with Hong Kong Land:

- Majority of the assets are concentrated in Hong Kong

- Jardine Matheson holds a majority stake

Majority of the assets are concentrated in Hong Kong

Depending on your world view, you either love or hate Hong Kong.

If you love it, you’ll remember the Hong Kong of old – vibrant, dynamic, and financial hub of Asia.

If you hate it, you’ll look at the rise of China, the oppression of the domestic population, and the flood of mainland Chinese.

Both are equally right.

My personal view – I think Hong Kong will remain relevant for years to come.

The common law system, freely exchangeable currency, and the existing financial and legal infrastructure will take many years to be replicated in Mainland China.

But I’m not going to paint an overly rosy picture of Hong Kong. The future to me lies across the causeway, in the gleaming skyscrapers of Shenzhen, Guangzhou and Shanghai.

The best days for Hong Kong are probably past.

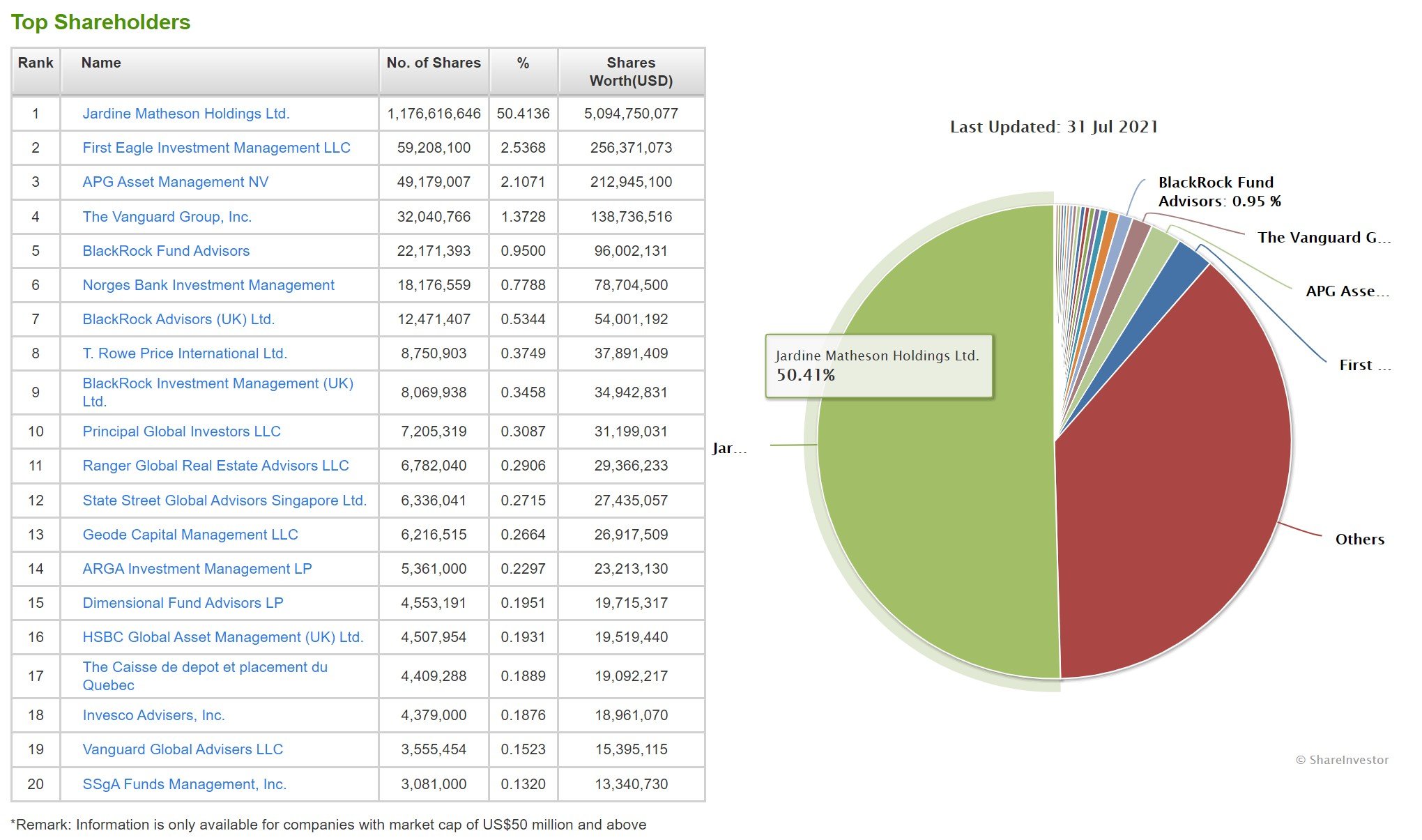

Jardine Matheson holds a majority stake

Jardine Matheson was one of the original Hong Kong trading houses that date back to imperial China and then the British era.

That’s how far back it goes.

Jardine Matheson holds a majority (50.4%) stake in Hong Kong Land, which means that everybody else is just a minority shareholder, with very little decision making rights.

To me, that’s probably one of the main factors holding it back.

If you can have an activist investor come in to shake things up – jostle the board to sell some assets to unlock value, or do what CapitaLand did, perhaps this dividend stock can trade at a better valuation.

But for now it looks unlikely.

When I last looked at Hong Kong Land in 2019, it was trading at 0.33x book value, at $5.4.

If you bought back then, even after factoring in the dividend you’ll still be losing money ($4.33 today).

And that’s really the problem with Hong Kong Land.

It’s cheap, and has a high yield. But there’s also a reason why.

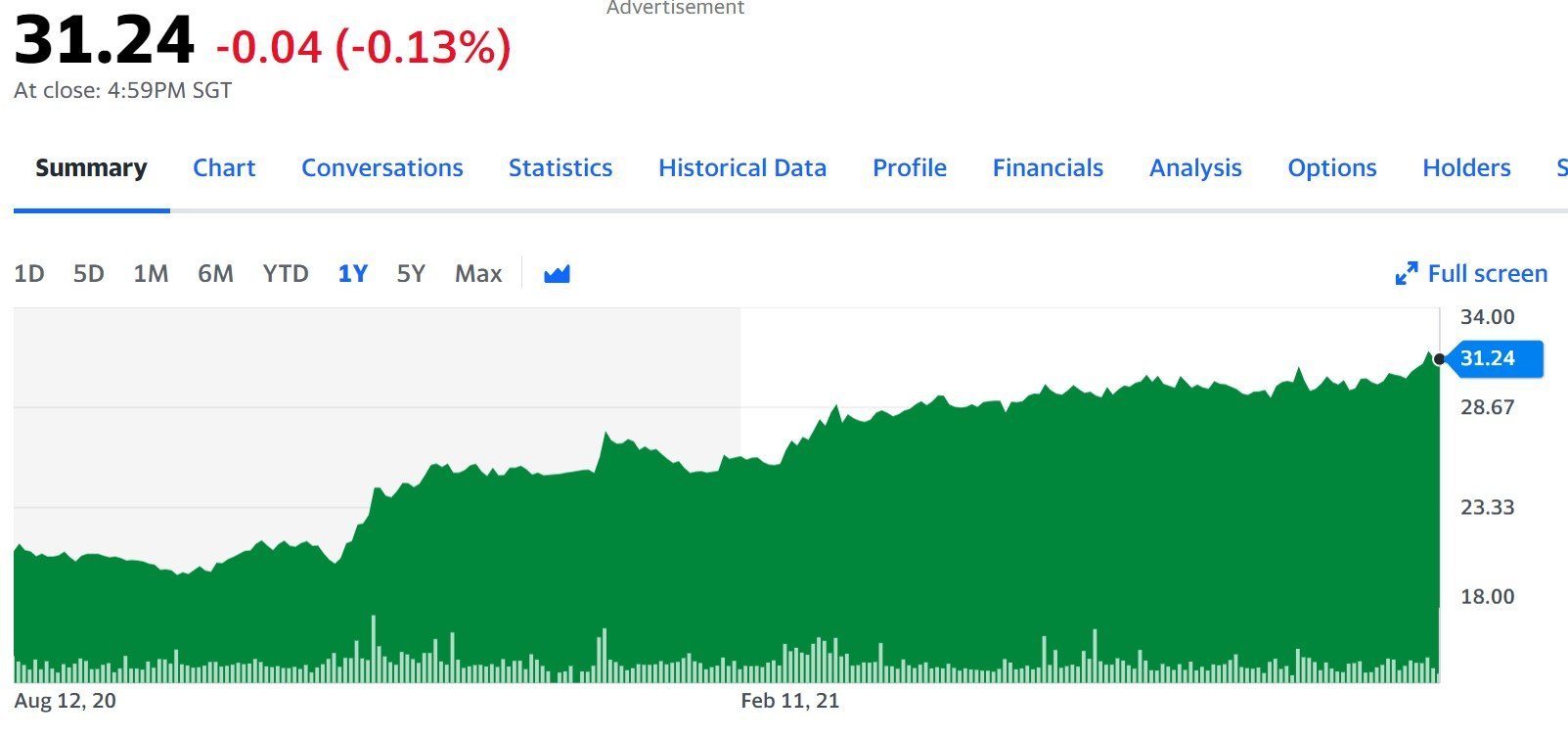

2. DBS Bank (SGX: D05)

Stock Price: 31.24

Price / Book: 1.5x

Trailing Dividend Yield: 2.31%

Forward Yield (estimated on 33 cents 2Q dividend annualised): 4.2%

DBS Bank. Need I say more?

MAS has removed the dividend cap for banks, so if we take the latest 2Q dividend of 33 cents – that works out to a 4.2% annualised dividend yield, based on today’s price.

Which is frankly very high, considering most cash savings accounts pay below 1% today.

In fact you can get a 3x higher yield putting your money in DBS stock, than in a DBS 1 year fixed deposit (1.15%). Crazy right?

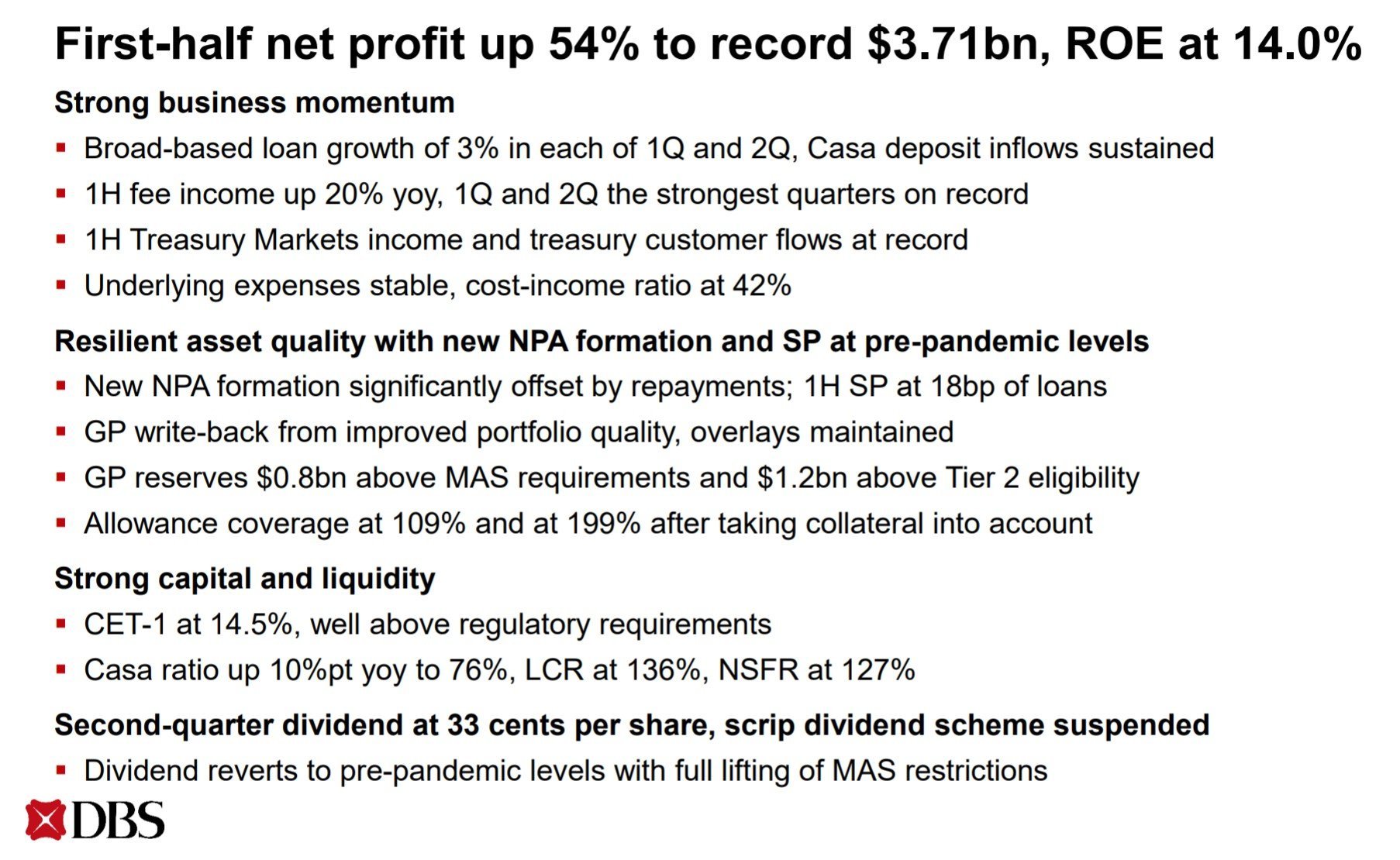

How strong is DBS’s business?

Latest financials below, and it’s rock solid.

Broad based loan growth, fee income up, costs under control, capital ratios rock solid etc.

Are interest rates going up?

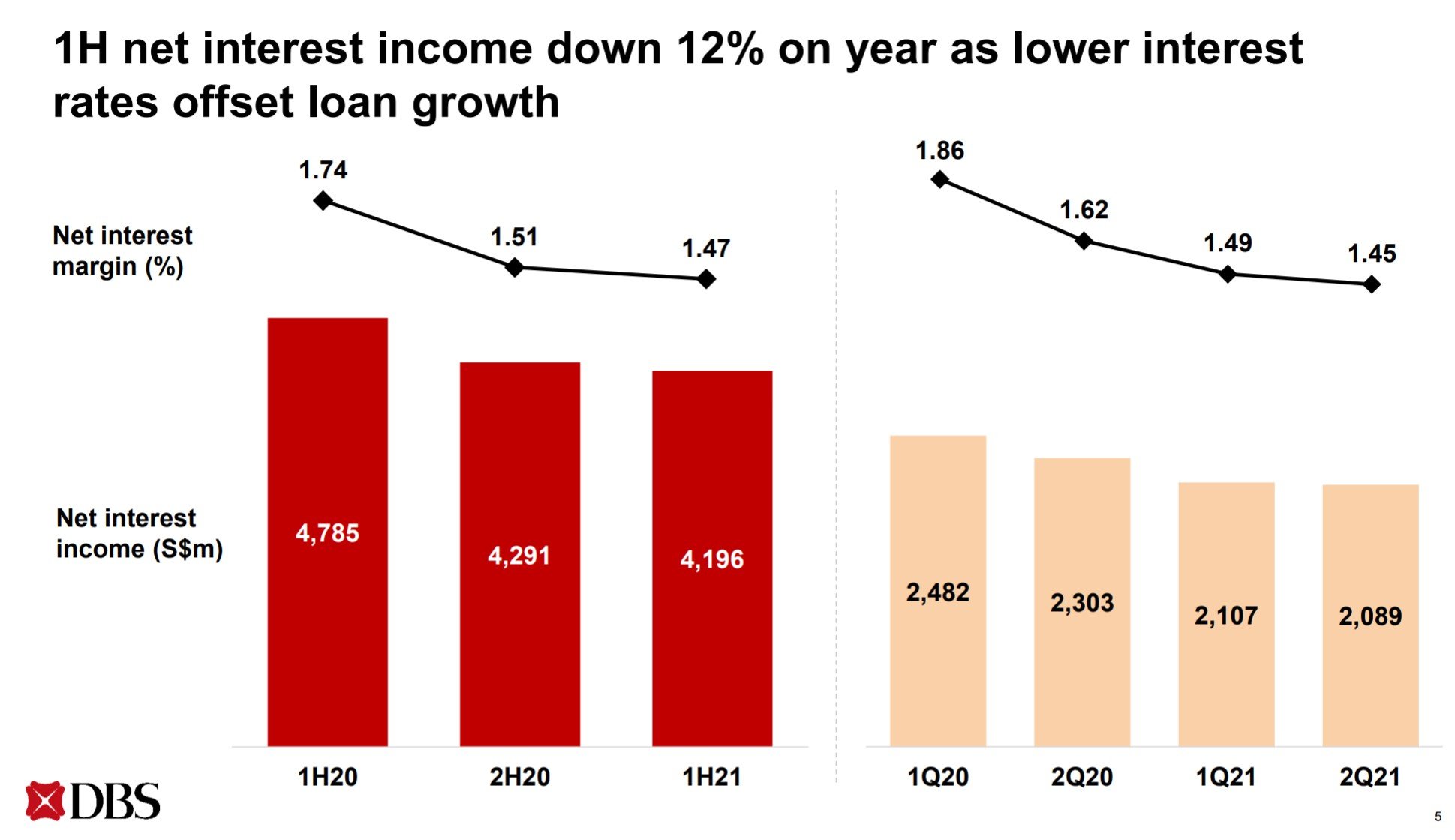

The only one problem, is the low interest rates.

So even though DBS has been growing their loan book, net interest income has still come down because interest rates are lower as compared to 2020.

I don’t think this is a big factor, because going forward I see interest rates going up.

Which could translate into a big earnings boost for DBS Bank.

Is it time to take profits in DBS?

A lot of investors have been asking whether it’s time to take profits in DBS.

If you bought at the $16 – $18 range last year, you’re sitting on close to 100% profits now. And a 6%+ yield on cost.

I know it’s crazy high compared to last year, but if interest rates are going up, there could still be room to run in this dividend stock.

I’m still holding on to mine in any case.

3. CapitaLand Limited (SGX: C31)

Stock Price: 4.09

Trailing Dividend Yield: 2.2%

CapitaLand’s shareholders just approved a big restructuring.

Long story short – the development business is going to be privatised at book value. Going forward, the listed CapitaLand will only hold developed assets, and the listed REITs like CICT and Ascendas REIT.

I really like this transaction – and the market clearly agrees because the share price has been on a tear ever since.

At today’s price, you’re buying in at about book value.

Dividend yield is tough to estimate, but I would put it at approximately 3-4% going forward.

Ideally I would want to buy in at a 10% discount to book value, but given how high quality CapitaLand’s property portfolio is, I think current prices are fine.

If you look beyond the next 6 – 12 months (which is still quite uncertain), and you look at 2 to 3 years out, I think there’s a very good chance we’re going to be living in a more inflationary world.

And high quality real estate is one of the best hedges to inflation.

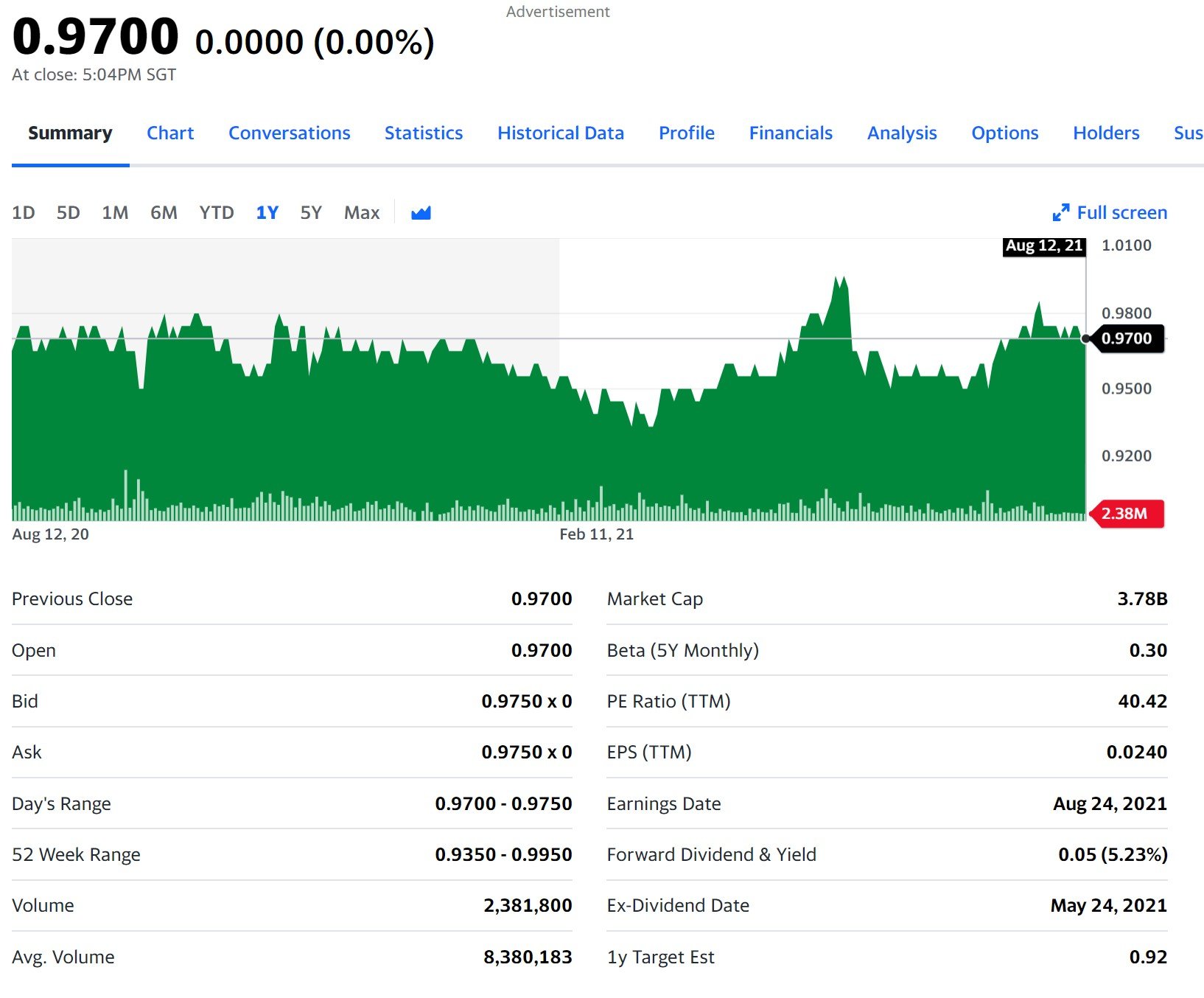

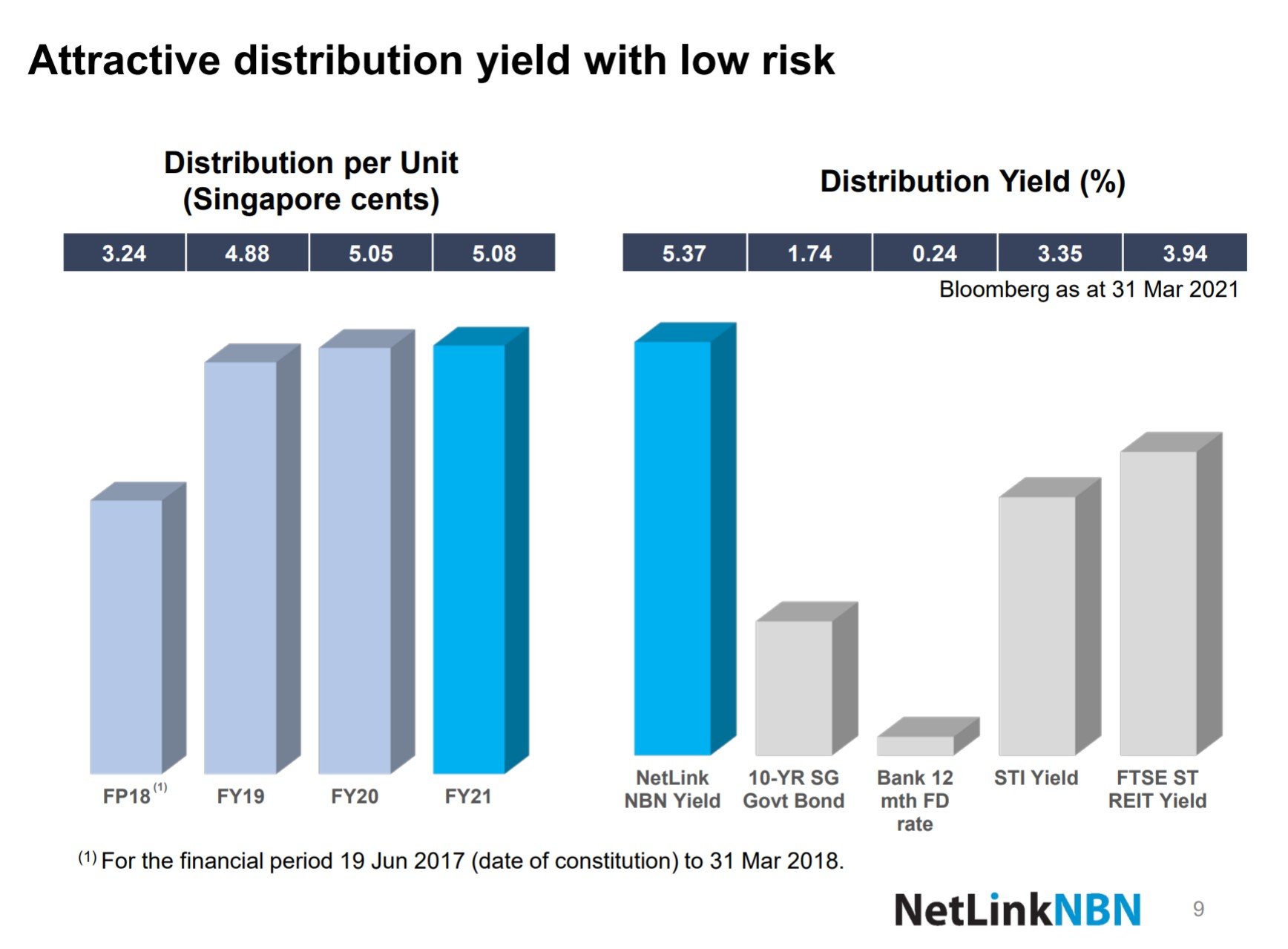

4. Netlink Trust (SGX: CJLU)

Stock Price: 0.97

Trailing Dividend Yield: 5.2%

Netlink trust is as pure a Singapore dividend stock as it gets (okay business trust to be precise).

It trades at a 5.2% dividend yield, with a rock solid dividend – but don’t expect much growth going forward.

Netlink trust owns a majority of the fibre connection in Singapore.

Each time you pay a fee to have fibre broadband set up in your home, and each time you pay the monthly fee to Singtel, a portion of that goes to Netlink.

Prices are tightly regulated by IMDA, so don’t expect price increases beyond inflation.

And almost 90% of homes in Singapore are on Fibre today, which also means any growth will have to come from population growth.

Like I said – the yield is good, but don’t expect much growth.

In fact as interest rates go up, there could be some risk of capital loss.

Because of how rock solid the dividend is, leverage is an option here. Throw in a 30% leverage and you could already be looking at a 7-8% dividend, which is very, very juicy in this market.

You do need to have good risk management if you want to use leverage though.

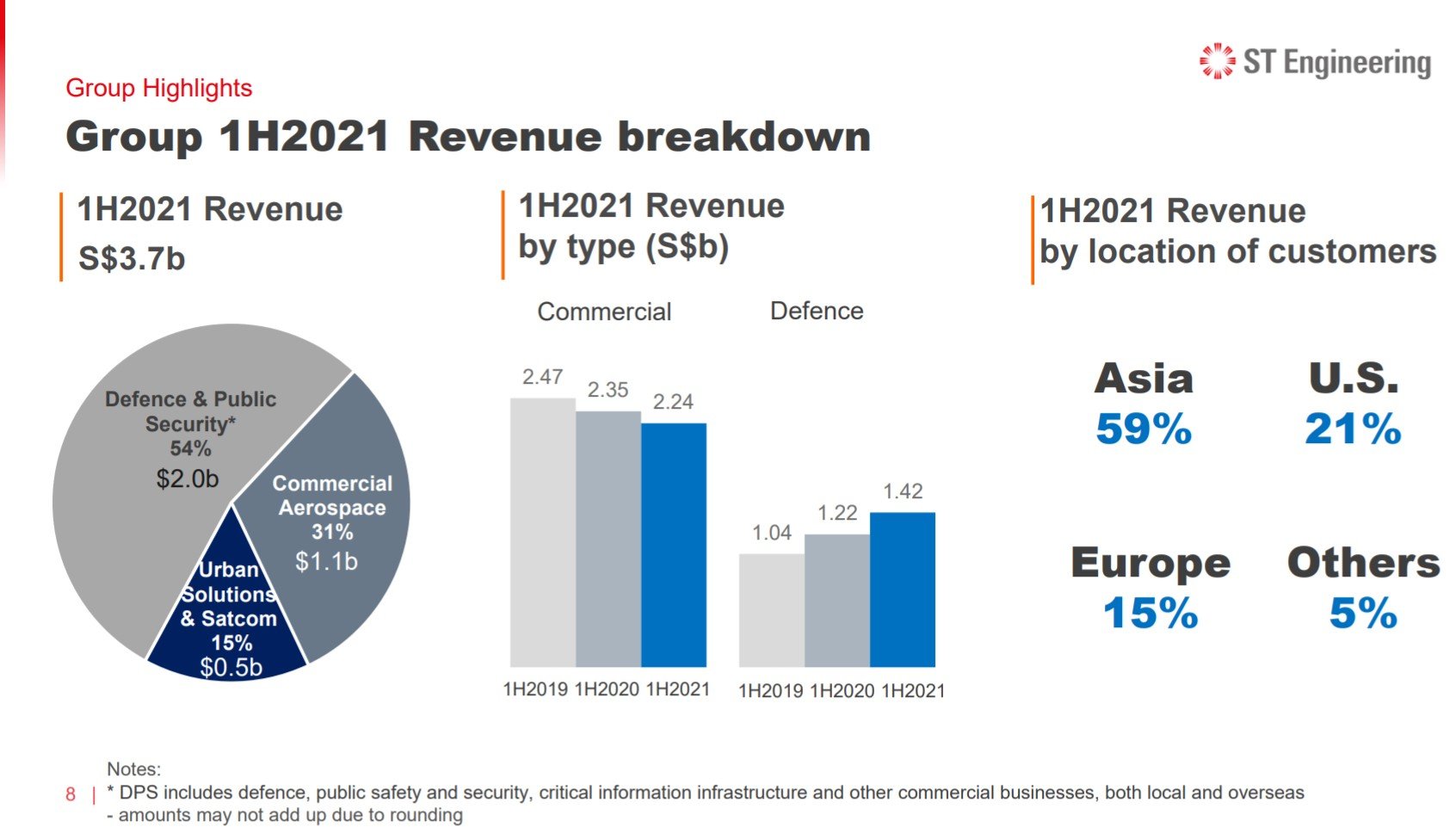

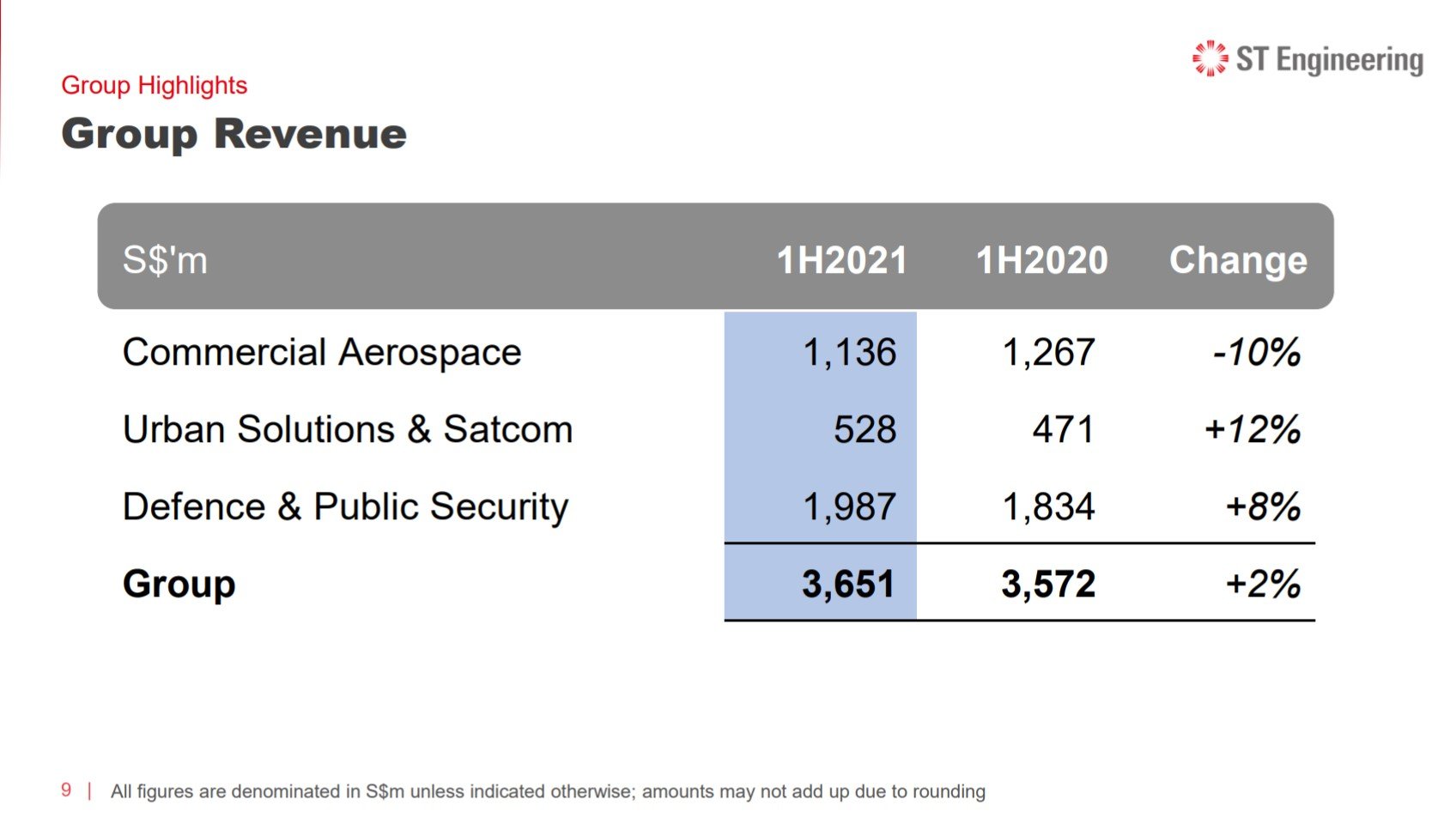

5. Singapore Technologies Engineering Ltd (SGX: S63)

Stock Price: 4.08

Trailing Dividend Yield: 3.67%

Dividend Payout Ratio: 90%

ST Engineering is split into 3 segments:

- Defence & Public Security

- Commercial Aerospace

- Urban Solutions

The guys will know ST Engineering as the manufacturer of our “beloved” SAR-21.

Because of COVID, the aerospace business has been hit, but the urban solutions and defence businesses are resilient enough to pick up the slack.

That’s the benefit of having a diversified business like this.

The dividend yield of 3.67% has a 90% payout ratio, which is slightly worrying.

There is risk of a dividend cut if the core business is impacted.

However, I still think we are in the early to mid stages of this cyclical upturn. So the chances of a big cyclical downturn hurting earnings is not big.

And as things go, ST Engineering’s business is not as vulnerable to disruption as the likes of Singtel or Keppel or Sembcorp Marine.

We recently did a deep dive into ST Engineering, so check it out for more details.

Honourable Mention: Other High Dividend Singapore Stocks

Now on to some very strong honourable mentions – for a bunch of great Singapore high dividend stocks that almost made this list.

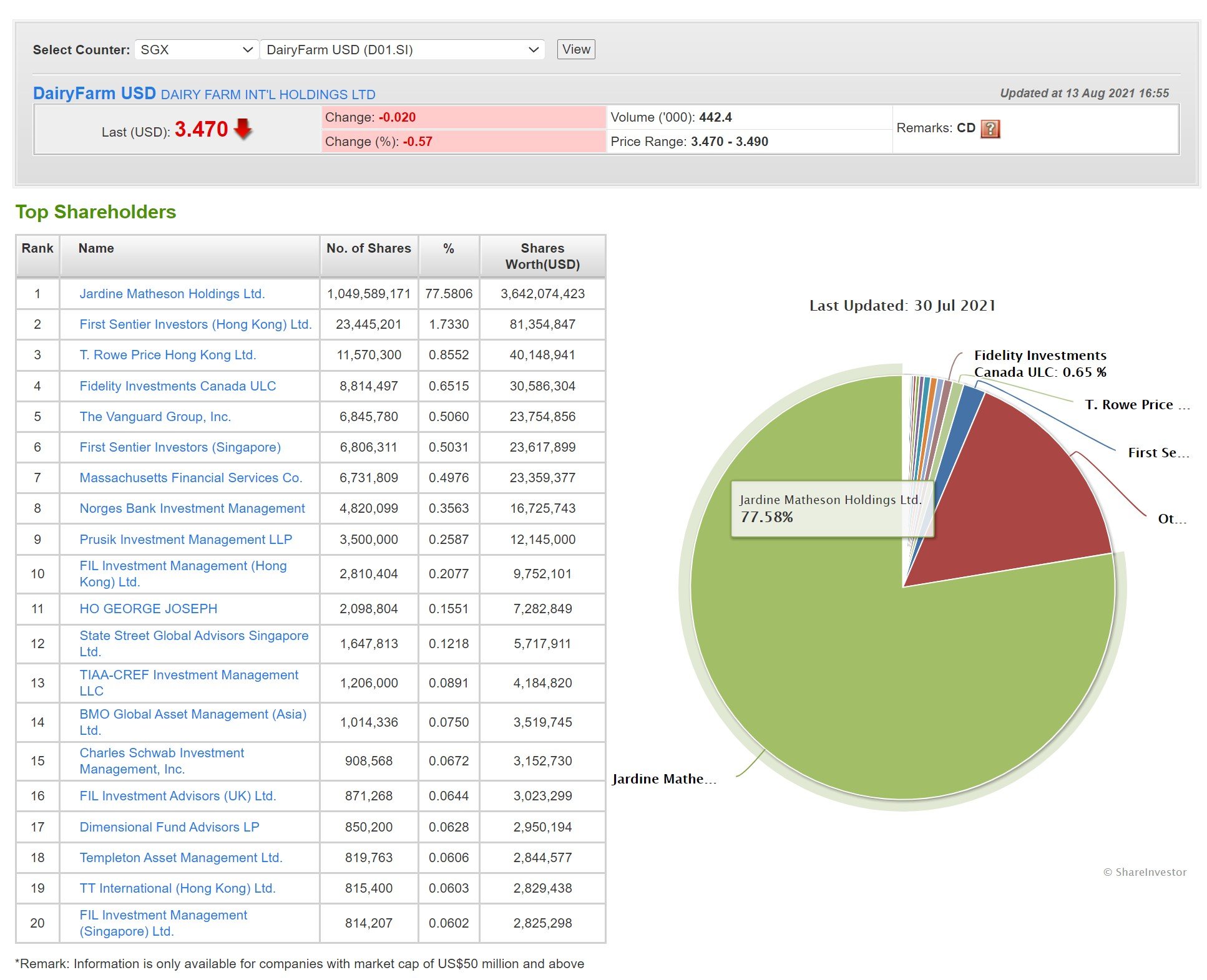

Dairy Farm International Holdings Ltd (SGX: D01)

Dairy Farm International owns Cold Storage, Giant, 7-Eleven, Meadows, Guardian.

You would have expected them to do well from COVID, but the share price has been a disaster recently:

Current dividend yield is a very strong 4.7%.

But Dividend payout ratio is worrying at 90%.

My concern with Dairy Farm is two-fold:

- Secular disruption from tech and changing retail patterns

- Jardine Matheson the majority shareholder

Secular disruption from tech and changing retail patterns

Probably the most troubling one.

Consumer patterns are changing rapidly, and technology / eCommerce has dealt traditional retail models a deathblow.

I’m not sure if Dairy Farm Holdings will adapt well to this new reality.

Jardine Matheson the majority shareholder

Just like Hong Kong Land, Jardine Matheson is the majority shareholder.

77.5% in this case.

I don’t like this for the same reasons as Hong Kong land.

Big Oil

It’s probably not cool to admit given that ESG is all the rage – but I’m a big oil bull (horse?).

Everybody is talking about moving to renewables, while forgetting that the transition is going to take time. Those cars are not going to switch to electricity overnight, nor are the planes.

At some point in time, as the world reopens, the underinvestment into oil over the past 12 months is going to come back to haunt us.

I loaded into oil positions last year, and while I’m up handsomely, I still think there is room to run.

The oil majors like Shell (RDSB on the London Stock Exchange for no withholding tax) trade at a 4.6% yield today, with potential of capital gains if oil prices go up.

Venture Corporation Ltd (SGX: V03)

Venture is a global provider of technology products and solutions. It is best known for its superior capabilities in Original Design Manufacturing (ODM) and providing high-mix, high-value and complex manufacturing.

I’ve heard a lot of good things about Venture Corp.

And at today’s price, it comes with a juicy 3.84% dividend yield too.

Unfortunately I’ve never had a chance to do a deep dive, so I don’t know enough to comment constructively on Venture.

If you know anything just let me know in the comments below!

Closing Thoughts: Top 5 high yield dividend stocks to buy in Singapore

And there you have it – Top 5 high yield dividend stocks to buy in Singapore.

It’s not a comprehensive list by any means, so if I missed out any gems just let me know in the comments below.

Full disclaimer – I hold positions in CapitaLand, DBS, Netlink Trust and Royal Dutch Shell.

What I would add, is that I think the path that lies ahead is one of higher interest rates.

The Feds are all but set to announce tapering this year, with a real possibility of rate hikes in 2022.

The short-term bottom for interest rates is probably close, if not already.

If you’re overweight on growth stocks, rising interest rates could spell trouble for your portfolio. Locking in some profits and rotating into other asset classes may not be a bad idea.

As always – my personal portfolio can be found on Patreon, and it’s a fairly even mix between growth and dividends today.

You can also check out Patreon for my latest stock watch, and more exclusive articles like this.

Love to hear what you think!

Last Weekend for National Day Promo for FH Courses! Sign up now to enjoy the big discount.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with and fund $2000.

Get 2 free Pfizer shares and 5 Haidilao shares (worth $200) you’re new to and fund $2700 + fulfil the trading conditions.

Special account opening bonus Saxo Brokers too (drop email to [email protected] for full steps).

Check out our review on Tiger Brokers and MooMoo.

Since you asked for comments on Venture, a quick one here. Was in the tech industry but I don’t invest in EMS and subcon share. Margin is thin, needs high volume to be profitable. Bulk of profit go to the ODM / OEM. EMS / subcon works on project / product basis. Example, those who supply to Nokia, Blackberry previously, some faded together with the products. Apple killed many of them. Need to constantly win new businesses in accordance to the respective product life cycle and cope with rapid technological changes to survive.

Just my 2 cents, not a recommendation.

Thanks! Appreciate the sharing. 🙂

The playbook for Singaporean investors seeking dividend yield tends to be 1) big 3 local banks, 2) REITs, and 3) Netlink trust. The rest all seem to have some caveats regarding the competitive environment and their ability to sustain dividend payouts. Pre-pandemic I was considering SATS and SBS transit, but not sure how long it will take for earnings to return to normal levels. Elsewhere, VICOM also looks pretty okay as a steady dividend payer.

I was hoping you could share your thoughts on how Singaporean investors can seek yield globally. For myself, I would only narrow this list down to stocks listed in HK and London, as other jurisdictions require payment taxes on dividend income.

Like you, I also own RDSB. Others on my watch list are the big mining players BHP and RIO. In HK, the big 4 Chinese banks (issues on asset quality and national service) and the big Chinese Telcos (again issues of National service!) come to mind.

Was wondering if you had other ideas :).

Yeah Oil and China banks would be what I would look at. Oil is more a capital gains play to me, it’s not a counter I want to hold for 5 years or more given all the talk about ESG and renewables. China banks, well it’s really a leap of faith, on whether you believe the CCP will bail them out if anything goes wrong. I hold some, but position sizing definitely matters.

Apart from that REITs would be the big one frankly. Singapore’s REIT market is very developed today, and you can get very good exposure to global real estate via Singapore REITs.

That’s about it really. Commodities is interesting. I think like oil, they’re good to play a possibly cyclical upturn if we get more inflation, but longer term I wouldn’t want to hold them too (just flip for capital gains).

But that’s enough options for dividend stocks for me. Use the above to form a dividend portfolio, and then allocate generously to growth plays as well. The world is changing very quickly, so some allocation to growth stocks is required as well.

Ah thanks for your comments. No problems on the growth portion for me though! Too many ideas and not enough capital :).

As I age towards retirement I am struggling more with where to find decent and fairly safe yield!

With regards to dividend yielders two additional points noting that you indirectly allude to in your article and comments.

First, the ability of a company to grow dividends over time. (The so called dividend “kings”/“aristocrats” method). I guess this is just the other side of the coin of earnings growth / capital appreciation.

Second, different dividend yielders exhibit different sensitivity to inflation. For cyclicals and banks, inflation (and higher interest rates) are good. For REITs, it depends because cost of funding and rentals both go up. Hence, my initial question above on diversifying the sources of one’s dividend yield as much as possible!

Haha hear you on the growth stocks.

Agree on both points you raised. We live in an era of technological disruption, so the concept of buying a dividend stock today and expecting it to raise dividends for the next 30 years is going to be very tough to execute. Take Google for example – given how quickly the internet is evolving, how sure are we that google will still be relevant 10 years from now?

This also looks to be the golden decade for macro investing. The past decade was about central bank liquidity – so passive ETFs was the best way to capture that return. Going forward, inflation may make a comeback, with varying impact across asset classes. So active investing may start to generate more alpha vs passive indexing. FT had a great article on this, v interesting if you have a subscription: https://www.ft.com/content/c87d52b2-d54e-4dae-9b50-98ca1e6c1d4c

I suppose the risk with Net link trust is share price dropping when interest rate rises. Other than that it’s a solid return, low volatility counter.

As for HKland, it’s probably the cheapest STI blue chip at 0.3NAV. So we’re waiting for them to unlock the value somehow – any form of monetisation of their assets.

Yup agreed on Netlink. There’s some risk of capital loss depending on how quick and how fast interest rates go up. And unlike REITs there’s less opportunity for capital gains from real estate price appreciation.

Agreed on HK Land. Very cheap, and very big dividend. But hard to see what would be the catalyst near term. You do get paid to wait though.

I’m of the same opinion on oil and gas, that the under investment is going to come back and bite us in higher prices. Also, that many are underestimating how challenging it will be to move away from oil and gas.

Unfortunately, the market is not appreciating this at the moment. I am also holding onto some oil and gas stocks, wondering if I’m too early and should I be stubborn or admit that the market is smarter than me.

Such is investing, think in probabilities but outcome is binary

Haha I guess the timing matters too. I picked up most of my positions last year, so they are still up 50% – 100% for me.

Short term looks to be rough with the delta variant and Fed tapering, but this oil underinvestment thesis is more of a 1 – 2 year play. So we need to give it some time to play out, and ride out the short term.

Hi, I’m new to stock.

May I know what kind of platform is safe and lower risk for people who is going to start investing?

Hi you can check out our guide to investing articles here: https://financialhorse.com/guide-to-investing/

Really depends on your risk appetite – Singapore Savings Bonds for risk free, blue chip REITs for medium risk, small cap growth stocks for high risk etc.

Hi, saw Wilmar is in the list in your article, may I know what is your view on this company? From the past few years, the profit and dividend increased yoy. Thanks.

Haven’t looked into Wilmar closely frankly, so can’t comment unfortunately.