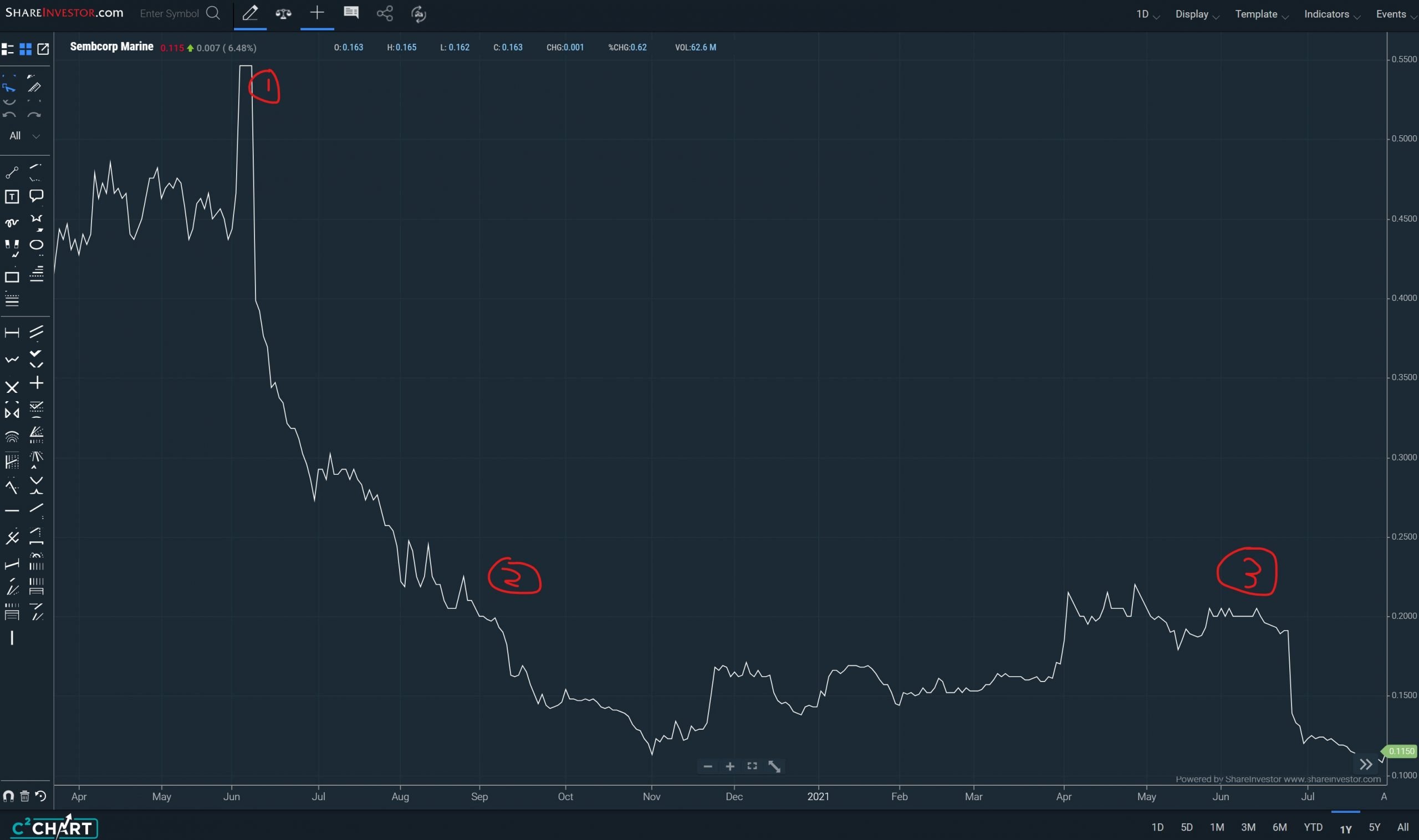

This is the 5 year chart of Sembcorp Marine.

It’s an absolute disaster – from a high of $1.75 in 2018, to $0.12.

Sure, there were a bunch of right issues that brings the average price down, but it’s still nothing short of value destruction for shareholders.

Since the latest announcement of (1) another $1.5 billion rights issue, and (2) merger with Keppel O&M, the share price has plunged another 50%.

Is there value in this stock? Or is it just a falling knife on it’s way to zero?

BTW – we share commentary on Singapore Investments every week, so do sign up for our mailing list.

Don’t forget to join our Telegram Channel and Instagram (or our Reddit Community)!

[mc4wp_form id=”173″]

Timeline of Sembcorp Marine

3 big events for Sembcorp Marine in the past 12 months:

(1) June 2020 – Sembcorp Marine announces a demerger from Sembcorp.

Sembcorp Marine launches a massive 5 for 1 rights issue (to raise $2.1 billion). Rights issued at $0.2 per share (share price at the time was 0.56).

Sembcorp Industries jumped 40%, and Sembcorp Marine dropped by 27%.

(2) Sep 2020 – Demerger of Sembcorp Marine from Sembcorp Industries is completed.

(3) June 2021 – Sembcorp Marine announces another $1.5 billion rights issue (barely a year after the first). Rights issued at $0.08 vs market price of $0.19.

Sembcorp Marine and Keppel O&M announce they will to merge into 1 entity. Details to be released by end of 2021.

Read more on my analysis of the Sembcorp Marine / Keppel O&M merger here.

What does Sembcorp Marine do?

Sembcorp Marine provides services to the offshore marine sector.

Think oil rigs, offshore platforms, specialised shipbuilding etc. The slide below gives you an idea of the kind of projects they take on.

Business is global, via shipyards in Singapore, Indonesia, UK and Brazil.

Just like Keppel and Sembcorp, Sembcorp marine is trying to go into the renewables space, which they see as the future.

Financials of Sembcorp Marine

Note: The research for this article (and most of the charts) are sourced from ShareInvestor Webpro. The platform offers 10 years of financial data across 7 markets, along with charting tools, screeners, insider trades, consensus estimates and more!

From 10 – 14 August, ShareInvestor is running a limited time promo. Find out more here!

So I pulled up the 8 year financials from Shareinvestor Webpro.

It’s a real disaster.

Key takeaways:

- Sembcorp Marine has been losing money ever since the first oil crash in 2015

- Margins never recovered from 2015. They were about 9% pre-2015, but after 2015 it has been 0 to negative.

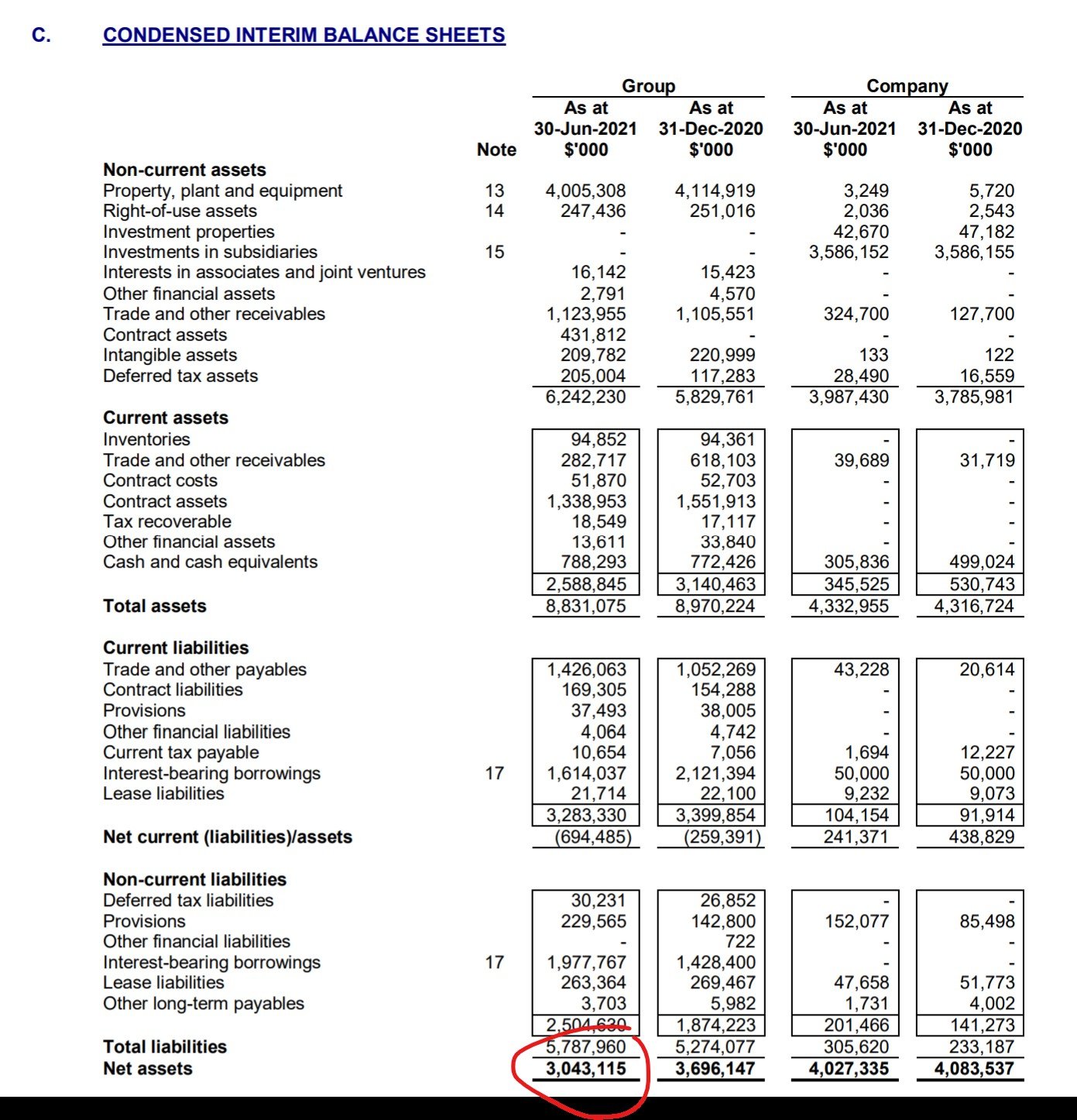

Book Value of Sembcorp Marine

Latest Book Value from Webpro puts it at about $0.27, which means Sembcorp Marine is trading at about 0.42x book value.

I checked this against the latest balance sheet which puts book value at about $3.04 billion.

With the current market cap of $1.42 billion, Sembcorp Marine trades at about 0.47x book value.

But what is the true value of Sembcorp Marine’s assets?

The bigger question – what is the true value of Sembcorp Marine’s assets?

Don’t forget most of this is marine equipment – ship building yards etc. If you sell them on the open market today, it’s very unclear how much a potential buyer would be willing to pay for them.

So I wouldn’t place too much emphasis on the book valuations.

It’s not about how much you can sell it for parts, more about how much cash flow you can generate from it.

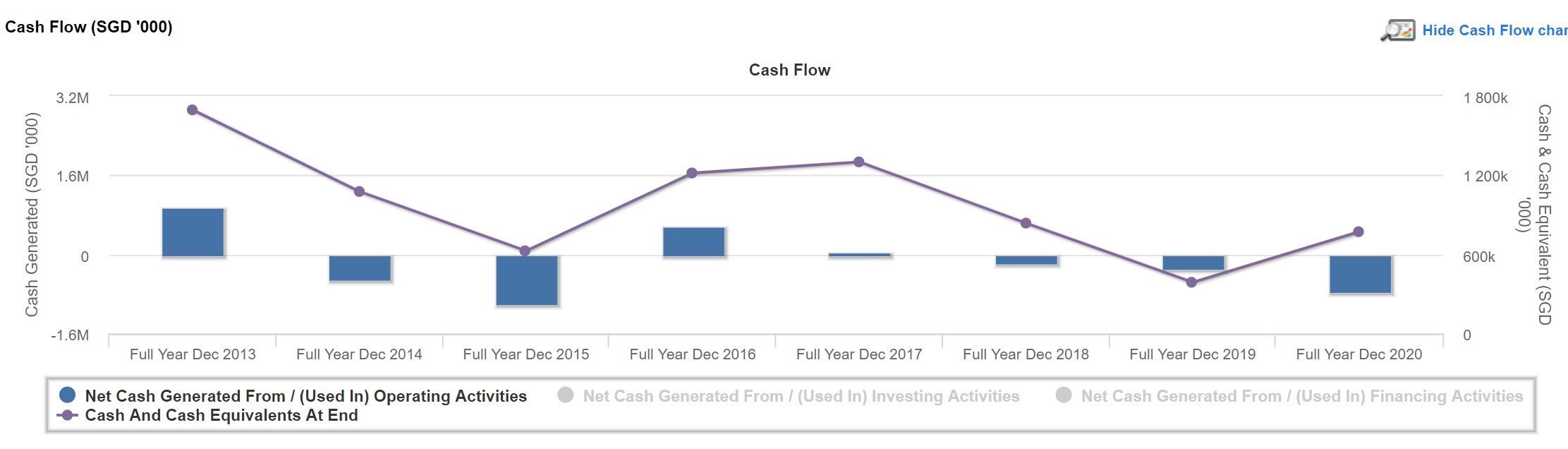

Cash Flow of Sembcorp Marine

Cash flow is almost as bad as the financials.

Sembcorp Marine has been bleeding cash almost every year since 2015.

Interestingly, their cash position is decent, with almost $800 million in cash on hand at end 2020.

The problem is that most of this cash doesn’t come from the operating business, but from financing.

Sembcorp Marine has been raising money from shareholders and borrowing from banks to keep the operations afloat.

Not good.

Sembcorp Marine Rights Issue and EGM on 23 August 2021

Sembcorp Marine will have an EGM on 23 Aug 2021 to approve the rights issue.

So if you buy into Sembcorp Marine shares today, do note there will be a big rights issue coming.

For every 2 shares in Sembcorp Marine ($0.12), you will get 3 rights at $0.08.

At today’s price – for every $1000 in Sembcorp Marine, you are being asked to cough up $1043 in the rights issue.

That’s a massive capital raise, and very dilutive.

How sound will the Marine business be going forward?

The million dollar question for Sembcorp Marine is going to be the viability of the marine business.

No amount of financial engineering or merger with Keppel will be able to turnaround Sembcorp Marine, if the core business is not sound.

And that’s where it gets tricky.

There are 2 big issues that concern me:

- Strategically, can Singapore compete in the marine business?

- Operational Excellence – Can Sembcorp Marine deliver operational efficiencies required to excel in this business?

Strategy – Can Singapore Compete in the Marine Business?

In the heydays of Keppel and Sembcorp Marine, they were able to build ships and oil rigs cheaply, quickly, and with high quality.

Then came the rise of the China and Korean shipbuilders.

They relied on cheap manpower, state backed subsidies, and close connections to supply chains to deliver what Keppel / Sembcorp Marine used to do, but cheaper and better.

That to me, marked the start of the end for the Keppel O&M / Sembcorp Marine style business.

The question then is whether anything can be done today to turn that around.

And I’m really not sure.

Singapore competing in Fintech, Legal Services, Wealth Management I completely understand. But Singapore competing in Shipbuilding? Not so sure.

This isn’t the 1980s anymore. The world has moved on, and we may need to accept that reality.

The competition has state backed subsidies and armies of cheap manpower. They took the Temasek model and supercharged it. It’s hard to see whether Singapore can compete effectively against such competition – even with the merged Keppel O&M / Sembcorp Marine.

Operational Excellence – Can Sembcorp Marine deliver?

A lot of you pointed this out in the Singtel article, with old school businesses like this there are 2 ways to succeed.

First is to take the cash flow from the old world business, and invest it into new world businesses. Think Softbank using cash flow from the Telco business to invest into Alibaba. Or Reliance Jio building platforms in India.

The second is operational excellence. Deliver the exact same product as the other guy, but better, faster, and cheaper. To the point where your customers love you and will never leave.

Most businesses will end up in either one of these paths.

With Sembcorp Marine, the first is pretty much out. There’s only so much you can do to disrupt shipbuilding.

Which leaves the second – operational excellence.

Can Sembcorp Marine turn around the business, reduce costs, and gain efficiency?

Will the Sembcorp Marine / Keppel O&M merger help?

I suppose that’s the goal of the Sembcorp Marine / Keppel O&M merger. To reap these operational efficiencies.

The execution is going to be really tough though. They need to cut costs and make hard decisions going forward.

Comment from FH Reader

I received a fantastic comment from a reader on this:

Actually they got the business order not from 2 competing companies but as a whole team dividing orders shares. Example 1 team goes in for the deal and divides to 2 companies 60/40 or other values, Keppel always gets the bigger pie.

Although Marine companies tend to be messier than other industry, Keppel is a far better operating company compared to SM which is so messy like old Chinese Workshop especially their top management to Managerial positions. A few years ago when business began to be bad, they had reshuffled and left incompetent HOD/GM Managers who create a lot of havocs while the good Managers had left after mistreatment. From my experiences, they can ask contractors to work but will not pay up when job done, not like Keppel who is more honest in this case.

I can’t comment on how true this is, but it’s an interesting insight into Sembcorp Marine, and the interplay with Keppel.

It also hints at the operational challenges that lie ahead for the merged entity of Sembcorp Marine and Keppel O&M.

Why I would still subscribe for the Sembcorp Marine Rights Issue

Full disclosure – I don’t own any shares in Sembcorp Marine.

If I did though, I would still take up the rights issue.

In my view, the Sembcorp Marine rights issue at $0.08 is just too dilutive not to take it up.

If it were me, I would take it up to average down my price, and when price recovers in a few months I’ll probably sell it all. Unless the Keppel O&M merger surprises me (in a good way), I just don’t like the long term prospects for this industry.

That’s probably the best way to reduce losses here.

But frankly I feel bad for the Sembcorp Marine shareholders.

This chart is just pure shareholder value destruction.

What is the lesson from Sembcorp Marine?

Hindsight is 20/20, but as investors, what can we learn from Sembcorp Marine to ensure we don’t repeat the same mistake?

I narrowed it down to 2:

Bet on the right industry

A rising tide lifts all boats.

And on the flipside, a falling tide will affect all boats.

As investors, we always want to have secular tailwinds on our side, rather than against us.

I recall a report saying that investments into the small cap Oil & Gas sector for the past 10 years have seen capital losses of 83%.

Bet on secular trends of tech, big data, IOT, machine learning cloud etc. Sectors where the pie is growing.

Not ones with intense competition and a shrinking pie.

Within the industry – look for Operational Excellence

Once you identify the industry, look for companies that deliver operational excellence.

Companies that they deliver superior products at low cost, which high brand loyalty.

Think Walmart, Costco, Netflix, Amazon.

Here on Financial Horse, we’ve covered a ton of Temasek related restructurings recently. One point that stands out is that the Temasek Cos have fallen behind on both points. They have failed to bet big on the new world industries, and quality of execution has slipped in recent years.

The recent restructuring aims to address these issues, but it’s also clear that the task ahead is a herculean one.

Not all will succeed.

And as investors, it’s important to pick where to deploy our capital properly. Hope is not a plan.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list.

Don’t forget to join our Telegram Channel and Instagram (or our Reddit Community)!

[mc4wp_form id=”173″]

Dividend of Sembcorp Marine

Couple more points to look at, then I’ll share holistic views.

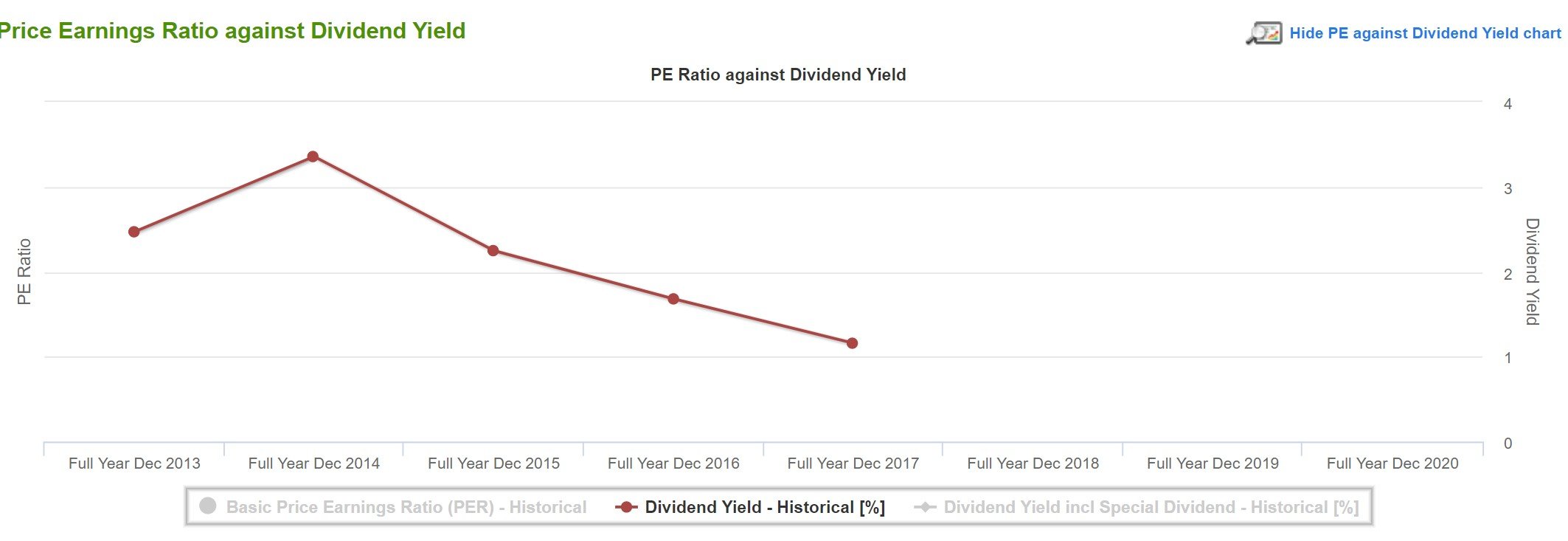

Sembcorp Marine hasn’t been paying a dividend since 2017, which is fair.

I don’t see how they can justify a dividend when the core business is bleeding cash.

Shareholders of Sembcorp Marine

Note: ShareInvestor WebPro is a great and very cost-effective way to do analysis like this – beats trawling through the SGX announcements one by one.

From 10 – 14 August, ShareInvestor is running a limited time promo. Find out more here!

Temasek is the single largest shareholder at 42%.

That’s a big percentage, but not as big as the others like Singtel or CapitaLand which are above 50%.

Would I buy Sembcorp Marine shares?

I don’t deny that Sembcorp Marine is very oversold short term.

RSI at 36 has recovered slightly, but is still very oversold.

Short term, once the rights issue is out of the way, and the Keppel merger news is announced, there could be a big bounce. There may be a tradeable opportunity for the traders out there.

But I’m a long term investor, and my time frame is measured in years not months.

And with the kind of timeframes I’m looking at – I’m really not sure about Sembcorp.

I think the broader strategy is tricky, I’m not sure if Singapore can ever be competitive in shipbuilding again. I also think execution is tricky – turning around the merged entity, reaping operational efficiencies, that’s going to require a lot of cost cutting and hard decisions to be made.

Not easy stuff.

My conclusion is probably similar to Singtel.

Promising, and worth monitoring. But for now, I see better opportunities for capital elsewhere.

If I had to give Sembcorp Marine a FH Horse rating, it’s probably going to be a 2 – 2.5 horse, depending on the timeframe. Short term this stock could be tradeable, longer term it looks tough.

Love to hear your thoughts!

Looking for a broker to buy China stocks? Get a Free Apple stock (worth S$200) when you open a new account with MooMoo or Tiger Brokers.

Special account opening bonus if you’re new to Saxo Brokers too (drop email to [email protected] for full steps).

Check out our review on MooMoo here.

More than 3 decades ago when Uncle play stocks, it was a $4 stock.

Take up the rights issue? Dont joke lah. The last time I touched it was for kopi money 4 years ago. Attended the AGM, the attitude really shocked me. Good bye forever.

Yeah I agree with this.

I think the rights issue is for shareholders who are still stuck. Because of how dilutive the rights issue is, the best bet may still be to take it up, and try to flip it a few months down the road once the Keppel merger news is out.

horrible, never looked at this sector bf so didn’t know valuation destruction so terrible. I think the only way to get out of the trap is refocusing on SG’s unique geo location, as a marine hub it still can offer lots of services to shipping or oil rig biz, but shipbuilding biz should be abandoned ASAP

That’s an interesting perspective. Question then would be whether Sembcorp can compete with the private players on cost/quality, and I suppose there’s no reason why they can’t. So perhaps there is a way out for Sembcorp Marine after all.

Hi,

can i seek some clarification, assuming that i hold 20k share.

If I were to subscribe, i will need to pay $1600 yea?

(20000 * 0.08) = $1600

what would be the outcome if i do not subscribe and i leave the share as it is. Will the existing 20k share become useless and not tradable?

For every 2 shares you get 3 rights.

So if you hold 20,000, you get 30,000 rights, which is $2400.

If you don’t subscribe, you will continue to hold the existing 20,000 shares, but your ownership of the company will be diluted because of the new i ssuance.

Ships aren’t going to disappear and oil rigs aren’t redundant yet. Marine hardwares, softwares and ancillaries have a sizeable continuation demand albeit no sustainable growth globally – but only companies having operational efficiency and product innovation could survive to harvest the yield. Financial engineering wouldn’t help the now dire state of Sembcorp Marine but the company could turnaround only with operational efficiency (not mere cost-cutting – amputating working hands and legs is suicidal) and move forward with product innovation (going into totally new products is costly without synergy and mostly suicidal).

True, I don’t disagree with this. The devil’s in the details though, I’m not sure if they actually get it done (the operational efficiency and product innovation).

If they can I agree Sembcorp Marine would be a buy.

Renounceable rights means it can be traded right? Any idea if it can be traded via CPFIS?

Yes renounceable is freely tradeable. Yes I believe Sembcorp Marine can be bought using CPF.

I have like 21600 rights to be exercise. All my shares previously are from iocbc with cash. So not possible to subscribe rights thru cpf right. It has to be in cash right?

Yup. If you bought in cash you need to subscribe in cash unfortunately.